Quick Summary: Computer Vision in Finance can reduce fraud exposure, accelerate onboarding, and strengthen compliance when deployed correctly. This guide explains real use cases, architecture, cost drivers, and partner selection criteria. You will gain clarity on implementation strategy, measurable ROI, and how to choose a development partner with confidence and control.

Financial institutions generate massive volumes of visual data across branches, ATMs, mobile onboarding flows, and surveillance systems. Many leadership teams still struggle to convert that visual data into measurable risk reduction and operational performance. Computer Vision in Finance gives executives like you a structured way to turn camera feeds and document images into actionable intelligence that supports fraud control, faster approvals, and stronger service efficiency.

Financial institutions invested 45 billion US dollars in artificial intelligence during 2024. Strong capital commitment signals confidence in automation programs. Many executives still question return on investment when pilots stall or integration delays slow deployment. AI Computer Vision in Finance must align with compliance, security, and measurable performance metrics.

CEOs and CTOs need clarity before selecting Computer Vision Solutions for Finance. Decision makers must understand how visual analytics connects to identity verification accuracy, queue management efficiency, and fraud exposure reduction.

This guide explains how to evaluate partners, avoid costly missteps, and implement Computer Vision Applications in Finance with confidence.

If you want to understand how computer vision actually works and implement it confidently but are unsure where to begin, read our complete Computer Vision Development Guide.

How Is Computer Vision Used in Finance Across Fintech Systems?

Computer vision in finance across fintech systems converts identity images, transaction visuals, and behavioral signals into structured risk scores, approval decisions, and operational alerts that integrate directly with digital platforms, compliance engines, and fraud monitoring systems.

Fintech platforms operate differently from traditional banks. Digital onboarding, instant lending, peer payments, and automated underwriting require real-time decision intelligence. AI Computer Vision in Finance supports that speed without compromising risk control.

Below is how implementation works inside fintech environments.

1. Identity Verification and KYC Automation

- AI Computer Vision in Finance extracts structured data from passports, national IDs, and driving licenses with high field accuracy.

- Face recognition models compare live selfie submissions against document photographs using confidence scoring thresholds.

- Liveness detection algorithms prevent spoofing attempts through motion analysis and texture validation.

- Extracted identity data passes through sanction list screening, politically exposed person checks, and internal watchlists.

- Risk engines generate structured confidence scores that determine automatic approval, manual review, or rejection.

- Full audit logs preserve verification steps for regulatory inspections.

KYC becomes measurable, traceable, and scalable rather than manual and inconsistent.

2. Fraud Detection Across Digital and Physical Channels

- Computer Vision Applications in Finance analyze behavior patterns across branch environments, ATM zones, and digital onboarding flows.

- Anomaly detection models identify suspicious movement clustering, repeated transaction attempts, or unusual dwell behavior.

- Understanding how computer vision works helps leadership teams see how video analytics combine timestamp data with transaction logs to detect coordinated fraud activity.

- Real-time alert systems escalate cases to fraud teams before transaction settlement.

- Continuous model retraining improves detection precision as fraud patterns evolve.

Fraud monitoring shifts from manual footage review to structured, intelligence-driven intervention.

3. Document Intelligence and Underwriting Automation

- Computer Vision Solutions for Finance extract structured data from loan applications, financial statements, tax documents, and compliance forms.

- Optical character recognition engines convert scanned documents into usable database fields.

- Data validation rules identify mismatched numbers, missing signatures, or altered values.

- Extracted data integrates directly with underwriting engines to accelerate approval decisions.

- Human review triggers only when confidence levels drop below defined thresholds.

Loan processing moves from manual data entry to automated decision support.

4. ATM and Self-Service Monitoring

- Computer Vision in Finance monitors ATM interactions to detect suspicious tampering behavior.

- Behavioral analysis models flag unusual transaction repetition patterns.

- Surveillance analytics identify skimming attempts through motion tracking around sensitive areas.

- Alerts integrate with central risk dashboards for immediate investigation.

ATM infrastructure gains real-time protective intelligence.

5. Branch Traffic Intelligence and Service Efficiency

- Use Cases of Computer Vision in Fintech include tracking visitor flow patterns across branch layouts.

- Movement heatmaps reveal peak demand zones and service congestion points.

- Queue analytics measure wait duration and service throughput rates.

- Interaction time metrics connect advisory sessions with product conversion outcomes.

- Integrated dashboards align visual traffic insights with CRM and transaction systems.

Branch operations gain measurable visibility instead of anecdotal feedback.

6. Compliance and Audit Support

- AI Computer Vision in Finance maintains traceable validation records for regulatory review.

- Document verification logs provide evidence trails for internal audits.

- Automated reporting simplifies compliance documentation requirements.

- Escalation workflows ensure high-risk cases receive structured oversight.

Compliance teams operate with structured proof rather than fragmented evidence.

Computer Vision in Finance delivers real value when visual intelligence integrates directly with risk systems, underwriting engines, compliance frameworks, and operational dashboards. Standalone analytics create visibility. Integrated systems create measurable control and performance improvement.

Where Do Computer Vision Applications in Finance Create Real Business Impact?

Computer Vision Applications in Finance vary across business models, yet every implementation must connect visual intelligence with measurable financial outcomes. The real value appears when visual data directly influences approvals, risk scoring, compliance validation, and operational performance, similar to how computer vision for industries drives operational precision across manufacturing, logistics, and retail environments.

Below is a practical breakdown across major financial segments.

1. Retail Banking

Retail banking environments generate continuous visual and document-based data across branches and digital onboarding channels.

- Computer Vision in Finance validates customer identity documents during account opening and verifies facial match through biometric comparison models.

- Branch surveillance analytics measure customer flow patterns, service demand peaks, and wait-time duration to improve staffing allocation decisions.

- ATM monitoring systems detect suspicious physical behavior, potential tampering attempts, and abnormal transaction activity.

- Visual data integrates with CRM and core banking systems to link service time, account opening duration, and transaction throughput metrics.

- Fraud detection models reduce manual review workload while maintaining regulatory compliance standards.

2. Corporate Lending

That processes involve large document volumes and high compliance sensitivity.

- AI Computer Vision in Finance extracts structured financial data from scanned balance sheets, income statements, and tax documents.

- Data validation algorithms identify discrepancies, altered figures, or missing signatures before underwriting begins.

- Automated field extraction accelerates credit risk evaluation and reduces document turnaround time.

- Visual audit trails store verification evidence to support internal and regulatory review processes.

- Integrated workflows push verified information directly into underwriting engines for faster credit decisions.

Corporate lending teams gain structured intelligence instead of manual document sorting.

3. Insurance

Insurance operations depend heavily on document validation and visual claim evidence.

- Computer Vision Solutions for Finance analyze uploaded images during claim submissions to detect damage patterns and validate authenticity.

- Image comparison models identify inconsistencies between reported damage and visual evidence.

- Automated fraud indicators flag suspicious claim behavior based on historical visual pattern analysis.

- Policy document extraction systems reduce administrative workload during underwriting.

- Integration with claims management systems enables faster investigation and settlement decisions.

It is improve claim accuracy while reducing false payouts.

4. Payments and Fintech Platforms

Digital payment systems require speed without compromising fraud control.

- Computer Vision in Fintech verifies customer identity during remote onboarding with real-time document and facial analysis.

- Behavioral pattern detection models monitor transaction flows to identify abnormal payment sequences.

- Visual dispute resolution systems analyze submitted evidence in chargeback scenarios.

- Compliance engines validate documentation automatically during high-risk transactions.

- Risk scoring models adjust transaction limits based on visual and behavioral analysis.

Use Cases of Computer Vision in Fintech demonstrate how embedded visual intelligence strengthens fraud prevention while maintaining transaction speed.

5. Wealth and Advisory Services

Advisory environments increasingly rely on remote identity verification and compliance monitoring.

- Computer Vision Applications in Finance validate investor identity during digital account creation.

- Document intelligence systems extract regulatory forms and disclosure data accurately.

- Video interaction analytics monitor compliance adherence during advisory sessions.

- Audit logging preserves verification history for regulatory oversight.

Advisory teams gain confidence in digital interactions without weakening governance controls.

Computer Vision in Finance creates impact only when visual analytics integrate directly with underwriting systems, fraud engines, compliance frameworks, and operational dashboards. While many computer vision examples highlight image recognition or object detection, financial institutions gain measurable value only when integrated intelligence delivers financial control and performance optimization beyond simple observation.

Use Cases of Computer Vision in Fintech That Strengthen Risk Control and Operational Intelligence

Use Cases of Computer Vision in Fintech go far beyond document scanning or facial verification. Real impact appears when visual intelligence becomes part of underwriting logic, fraud engines, compliance workflows, and operational monitoring systems.

Let’s walk through the most critical fintech use cases in practical terms.

1. Digital Onboarding and Remote Identity Verification

Digital onboarding forms the foundation of every fintech platform. Weak identity validation creates downstream fraud exposure.

- Computer Vision in Fintech extracts structured data from uploaded identity documents with field-level validation accuracy.

- Facial recognition models compare live selfie captures with document photographs using calibrated confidence thresholds.

- Liveness detection algorithms prevent spoofing attempts through motion analysis and depth validation checks.

- Extracted identity data automatically cross-verifies against sanction lists, watchlists, and internal risk databases.

- Risk scoring engines assign approval tiers, reducing manual review workload for low-risk customers.

- Full audit trails store verification steps for regulatory inspection and internal review.

Digital onboarding becomes faster, traceable, and compliant instead of manual and fragmented.

2. Fraud Prevention Across Payment and Lending Platforms

Fraud prevention remains one of the highest-cost risk areas in fintech operations.

- AI Computer Vision in Finance monitors suspicious behavioral patterns during onboarding and transaction initiation.

- Anomaly detection models identify unusual device positioning, repeated attempt sequences, or irregular submission timing.

- Video analytics combine session behavior with transaction metadata to detect coordinated fraud activity, moving beyond generic computer vision applications and examples into regulated financial risk environments.

- Real-time alert systems escalate high-risk cases before transaction settlement occurs.

- Continuous model retraining adapts detection logic as fraud tactics evolve.

It shifts from post-incident investigation to proactive prevention.

3. Compliance Automation and Regulatory Alignment

Regulatory oversight demands structured documentation and audit-ready evidence.

- Computer Vision Solutions for Finance validate uploaded documents against regulatory format and completeness standards.

- Automated consistency checks identify altered figures, mismatched signatures, or incomplete disclosures.

- Integrated compliance engines record verification history with timestamped logs for audit transparency.

- Escalation workflows route high-risk cases directly to compliance officers for review.

- Automated reporting dashboards summarize onboarding integrity metrics for internal governance teams.

Compliance operations gain measurable control without slowing customer acquisition.

4. Operational Monitoring and Performance Optimization

Fintech platforms require continuous visibility into workflow efficiency and system performance.

- Computer Vision Applications in Finance monitor digital interaction patterns to identify drop-off points during onboarding flows.

- Behavioral analytics detect friction points that reduce approval completion rates.

- Queue and support ticket pattern analysis reveal operational bottlenecks affecting customer experience.

- Integrated dashboards correlate visual behavior signals with transaction completion and revenue metrics.

- Management teams use structured performance data to refine process design and staffing allocation.

Operational intelligence improves without relying on guesswork or anecdotal feedback.

Fintech platforms operate in environments where customer acquisition, fraud control, and regulatory compliance must move together without friction. Computer Vision in Fintech creates real value only when visual validation strengthens risk accuracy while maintaining operational speed.

Identity checks, behavioral monitoring, and compliance verification must connect directly with decision engines instead of remaining isolated analytics layers.

Sustainable fintech growth depends on that alignment between intelligent automation and governance control.

What Are the Benefits of Computer Vision in Finance for Executive Teams?

Benefits of Computer Vision in Finance appear clearly when visual intelligence improves risk accuracy, accelerates decision workflows, strengthens governance transparency, and delivers structured performance data that leadership teams can measure and control.

Below is a practical breakdown of what those benefits mean in real financial environments.

1. Risk Reduction and Fraud Control

- Computer Vision in Finance strengthens fraud detection by identifying behavioral anomalies and document inconsistencies before transactions complete.

- AI Computer Vision in Finance reduces false positives through pattern learning that improves detection precision over time.

- Automated visual validation minimizes human error during identity verification and document review processes.

- Real-time alert systems enable risk teams to intervene earlier instead of investigating incidents after financial loss occurs.

- Integrated monitoring ensures that fraud signals connect directly with core banking and payment systems for faster response.

Financial institutions gain structured control over fraud exposure because visual intelligence supports prevention rather than post-incident analysis.

2. Faster Approvals and Reduced Processing Time

- Computer Vision Applications in Finance extract structured data from documents instantly, eliminating manual data entry delays.

- Identity validation engines automate facial comparison and liveness checks during digital onboarding.

- Automated field verification reduces document back-and-forth communication with applicants.

- Integrated workflows trigger underwriting decisions without waiting for manual document sorting.

- Processing speed improves without weakening compliance standards or review depth.

Approval workflows become predictable, measurable, and scalable under increasing transaction volumes.

3. Operational Efficiency Across Channels

- Computer Vision Solutions for Finance reduce manual review workload by prioritizing high-risk cases only.

- Branch analytics identify service bottlenecks through movement and queue monitoring.

- ATM monitoring systems reduce time spent reviewing surveillance footage manually.

- Automated document extraction decreases repetitive administrative tasks across lending and compliance teams.

- Structured performance dashboards replace anecdotal operational feedback.

Operational efficiency shifts from assumption-based management to evidence-based optimization.

4. Governance Visibility and Audit Readiness

- Computer Vision in Finance creates traceable audit logs for identity verification and document validation processes.

- Timestamped verification records simplify regulatory reporting and internal compliance reviews.

- Escalation workflows document every high-risk case review for governance accountability.

- Structured visual evidence reduces ambiguity during external audits.

- Compliance teams gain measurable oversight across digital and physical channels.

Governance teams gain defensible documentation instead of reactive explanations during regulatory inspections.

5. Data-Driven Executive Decision Making

- Visual analytics transform movement patterns, onboarding behavior, and document integrity signals into structured performance metrics.

- Leadership teams access real-time indicators that connect fraud exposure, approval speed, and operational throughput.

- Predictive models improve future risk forecasting based on validated behavioral data trends.

- Performance benchmarking becomes quantifiable across branches, digital platforms, and service units.

- Strategic planning decisions rely on verified intelligence rather than assumptions.

Computer Vision in Finance strengthens financial institutions when visual data moves beyond surveillance and becomes an integrated intelligence layer across risk, operations, compliance, and executive reporting systems. Organizations that align visual analytics with measurable business objectives experience controlled growth without sacrificing governance discipline.

What Is the Architecture Behind AI Computer Vision in Finance?

AI Computer Vision in Finance relies on a structured architecture that captures visual data, converts images into structured information, validates risk signals, and integrates results directly with financial systems that drive approvals, fraud control, and compliance oversight.

Many initiatives fail because leadership focuses on models first and architecture later. Strong architecture determines scalability, security, and measurable performance.

Below is how enterprise-grade Computer Vision in Finance is built.

1. Data Capture and Ingestion Layer

Financial institutions already operate camera systems across branches, ATMs, and digital onboarding channels. The first architectural responsibility involves structured intake of visual inputs.

- Cameras capture image and video streams in standardized formats aligned with processing requirements.

- Secure transmission channels encrypt visual data before sending it to processing environments.

- Edge devices filter unnecessary frames to reduce bandwidth and storage consumption.

- Metadata tagging attaches timestamps, device identifiers, and transaction references to every input.

- Retention policies define storage duration according to regulatory and governance standards.

A disciplined ingestion layer ensures downstream analytics remain consistent and auditable.

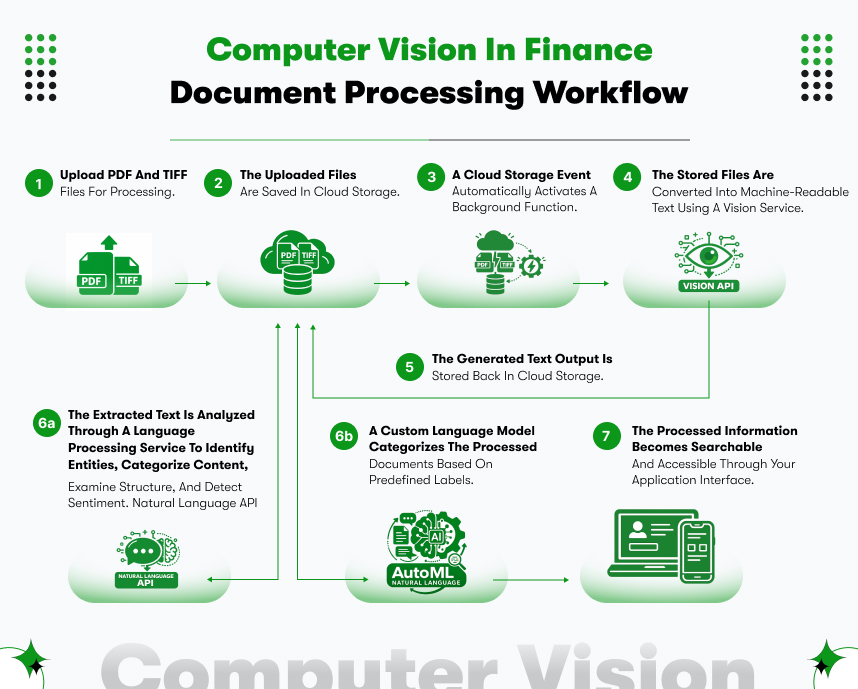

2. Image Processing and OCR Engine

Raw visual data must convert into structured fields before financial systems can use it.

- Optical character recognition engines extract text from identity documents, loan forms, and compliance paperwork.

- Image preprocessing modules enhance clarity through noise reduction and distortion correction.

- Biometric comparison models evaluate facial similarity using calibrated confidence scoring.

- Liveness detection algorithms analyze motion and depth characteristics to prevent spoofing.

- Behavioral pattern recognition models detect anomalies across surveillance feeds and transaction environments.

Model accuracy depends on domain-specific training data and continuous validation cycles.

3. Risk Evaluation and Decision Layer

Visual interpretation alone does not create value. Structured decision logic must follow.

- Extracted identity data cross-verifies against sanction lists and internal fraud databases.

- Risk scoring engines assign confidence tiers that determine approval, rejection, or escalation.

- Automated approval logic reduces manual review for low-risk cases.

- Escalation pathways route high-risk submissions directly to compliance teams.

- Audit logging records each decision stage for regulatory transparency.

Decision orchestration transforms visual insights into operational control.

4. Core System Integration Layer

Financial workflows rely on tightly connected systems rather than isolated analytics modules.

- Verified onboarding data integrates directly with account creation systems.

- Fraud alerts synchronize with transaction monitoring platforms in real time.

- Extracted financial document data feeds into underwriting and credit evaluation engines.

- Compliance validation logs connect with governance dashboards for oversight reporting.

- API frameworks maintain secure communication between AI services and financial applications.

Integration determines whether computer vision becomes operational infrastructure or remains a reporting tool.

5. Performance Monitoring and Governance Control

Sustainable deployment requires continuous oversight.

- Performance dashboards track detection accuracy, processing latency, and false positive rates.

- Drift monitoring systems identify behavioral shifts that require retraining.

- Access control policies restrict exposure to sensitive visual data.

- Governance frameworks define approval thresholds and escalation standards.

- Periodic audits confirm alignment with regional compliance regulations.

Computer Vision in Finance becomes enterprise-ready only when architecture supports scalability, security, and long-term governance discipline.

Architecture determines whether AI Computer Vision in Finance scales across enterprise systems or collapses under integration pressure. Financial leaders should evaluate architecture before evaluating model accuracy. Secure ingestion, structured processing, decision orchestration, and system integration must operate as one connected framework.

Weak integration creates isolated analytics that generate reports but fail to influence approvals, fraud control, or compliance enforcement. Strong architecture embeds visual intelligence directly into financial workflows, creating measurable performance improvement across risk, operations, and governance.

What Is the Implementation Roadmap for Computer Vision in Finance?

Computer Vision in Finance succeeds when execution follows a structured roadmap rather than experimental pilots. Strong planning prevents budget waste, integration failures, and compliance gaps. Below is a practical implementation path used in serious financial environments.

1. Define the Business Objective Before Technology Selection

- Leadership must clearly define whether the goal focuses on fraud reduction, onboarding acceleration, compliance strengthening, or operational visibility.

- Financial impact should be quantified through projected fraud loss reduction, reduced manual review cost, or faster approval turnaround.

- Risk tolerance levels must be documented so model thresholds align with governance standards.

- Compliance teams should outline audit requirements before technical architecture is finalized.

- Stakeholders across technology, operations, and risk functions must agree on success metrics.

Clear objective alignment prevents unnecessary feature expansion and scope confusion.

2. Conduct a Data and Infrastructure Assessment

- Existing camera systems should be evaluated for resolution quality, placement coverage, and consistency across branches or digital channels.

- Historical image datasets must be reviewed for accuracy, labeling quality, and suitability for model training.

- Secure data transmission protocols must be validated to protect sensitive customer information.

- Storage policies must align with regional regulatory retention requirements.

- Compatibility with core banking or fintech platforms must be technically mapped before development begins.

A structured audit avoids rework and unexpected integration challenges.

3. Develop and Validate Financially Aligned Models

- AI Computer Vision in Finance models must train on financial documents and real transaction environments rather than generic image datasets.

- Validation testing should include fraud edge cases and incomplete documentation scenarios.

- Confidence thresholds must reflect defined business risk tolerance.

- False positive and false negative rates should be measured before live deployment.

- Performance benchmarks must include processing speed and system load tolerance.

Model validation ensures operational reliability before exposure to real customers.

4. Integrate With Core Financial Systems

- Extracted identity data must connect directly with onboarding workflows.

- Fraud alerts must synchronize with transaction monitoring platforms in real time.

- Document intelligence outputs should feed underwriting engines automatically.

- Compliance logs must integrate with governance dashboards for audit transparency.

- API security layers must support high transaction volumes without latency issues.

Deep integration determines whether visual intelligence influences decisions or remains isolated from analytics.

5. Execute a Controlled Pilot Phase

- A limited deployment segment should be selected to test performance under live conditions.

- Measurable KPIs should track fraud detection improvement and processing time reduction.

- Compliance teams must review audit trail completeness during pilot execution.

- Operational teams should report workflow adjustments required during early deployment.

- Executive dashboards should provide real-time performance visibility.

Controlled pilots validate financial impact before enterprise rollout.

6. Scale With Monitoring and Governance Discipline

- Continuous performance dashboards must track detection accuracy and operational efficiency.

- Drift monitoring mechanisms should identify behavioral shifts that require model retraining.

- Governance reviews must ensure ongoing regulatory alignment.

- ROI tracking should compare actual performance against projected business case metrics.

- Structured feedback loops should refine workflows based on operational results.

Scaling converts Computer Vision in Finance from a project into a sustainable enterprise capability.

A structured roadmap protects investment, reduces compliance exposure, and increases the probability of measurable return. Computer Vision in Finance demands alignment between business objectives, data readiness, model validation, and system integration.

Leadership teams that approach implementation with discipline avoid stalled pilots and fragmented deployments.

A well-executed roadmap converts visual intelligence into operational infrastructure that supports fraud control, faster approvals, governance transparency, and scalable financial growth.

What Determines the Cost and Investment Factors for Computer Vision in Finance?

Cost discussions around Computer Vision in Finance often begin with model pricing. Real investment planning requires deeper clarity, especially when evaluating overall computer vision software development cost across architecture, integration, and governance layers. Architecture depth, integration scope, compliance requirements, and long-term monitoring determine financial commitment far more than model selection alone.

Estimated Cost Structure for Computer Vision in Finance

| Cost Component | What It Covers | Typical Investment Range (USD) | What Increases Cost |

| Business Analysis & Planning | KPI definition, risk mapping, compliance scoping | $10,000 – $40,000 | Multi-region compliance, multi-department alignment |

| Data Preparation & Labeling | Dataset cleaning, annotation, preprocessing pipelines | $15,000 – $80,000 | Poor historical data quality, large image volumes |

| Model Development | OCR models, facial recognition, anomaly detection systems | $30,000 – $180,000 | Complex fraud logic, multi-use-case deployment |

| Integration With Core Systems | API development, workflow automation, system orchestration | $35,000 – $250,000 | Legacy system complexity, real-time sync requirements |

| Infrastructure Setup | Cloud deployment, edge devices, storage architecture | $30,000 – $120,000 | On-premise deployment, high-availability setup |

| Security & Compliance Controls | Encryption layers, audit logging, bias testing, validation | $15,000 – $70,000 | Strict regulatory jurisdictions |

| Pilot Deployment | Controlled rollout, performance tracking, KPI validation | $20,000 – $60,000 | Multi-branch or multi-channel pilot scope |

| Ongoing Monitoring & Maintenance (Annual) | Model retraining, drift detection, performance monitoring | $20,000 – $150,000 per year | High transaction volume environments |

How Leadership Should Evaluate This Investment

Computer Vision in Finance requires capital discipline, not impulse approval. Financial leaders should evaluate investment against measurable risk exposure and operational inefficiencies.

- Fraud reduction initiatives should compare projected loss prevention against total deployment cost.

- Onboarding acceleration programs should measure revenue impact from faster customer activation cycles.

- Operational efficiency gains should calculate manual review cost savings across departments.

- Compliance automation should quantify reduction in audit preparation workload and regulatory penalty exposure.

- Integration depth should be assessed carefully because shallow integration weakens measurable return.

Total investment varies based on system complexity and deployment scale. Mid-sized institutions typically allocate between two hundred fifty thousand and seven hundred thousand dollars for structured implementation. Large multi-region financial institutions often invest significantly higher based on integration depth and governance requirements.

Cost discussion must remain connected to measurable financial impact. When leadership aligns scope with clear business objectives, Computer Vision in Finance becomes a structured capital investment rather than an experimental expense.

How to Choose the Right Development Partner for Computer Vision in Finance

Selecting a development partner for Computer Vision in Finance is a structural decision that affects integration stability, compliance posture, and long-term scalability, and many leadership teams begin that evaluation through structured computer vision consulting engagements to assess feasibility and risk alignment. Model accuracy alone does not determine success. Architecture depth, workflow alignment, and governance maturity define measurable outcomes.

1. Financial Workflow Alignment

- A capable partner understands how onboarding approvals move through compliance validation and risk scoring engines.

- Visual intelligence should connect directly with transaction systems, underwriting logic, and audit reporting frameworks.

- The partner must demonstrate familiarity with financial regulations that govern identity verification and fraud escalation.

- Prior deployments should reflect measurable operational impact rather than experimental proof-of-concept projects.

- Implementation discussions should revolve around business metrics, not only model performance percentages.

Financial workflow alignment reduces the probability of integration rework and governance friction during deployment.

2. Integration Engineering Depth

- Extracted document data must integrate automatically into onboarding and lending platforms without manual intervention.

- Fraud alerts should synchronize in real time with transaction monitoring systems across digital and physical channels.

- API frameworks must enforce encryption, authentication, and secure access control standards.

- Infrastructure planning should account for legacy core systems that cannot tolerate latency spikes.

- Scalable orchestration logic must support peak transaction loads without performance degradation.

Integration engineering depth determines whether Computer Vision in Finance influences real decisions or remains an isolated analytics layer.

3. Governance and Compliance Discipline

- Data handling practices must comply with regional regulatory frameworks across operating jurisdictions.

- Audit logging mechanisms should record each identity validation and escalation pathway clearly.

- Bias testing and fairness validation processes must protect institutions from regulatory exposure.

- Escalation thresholds should align with documented risk tolerance standards.

- Continuous compliance review cycles must remain part of long-term deployment governance.

Governance discipline protects institutional credibility and reduces regulatory vulnerability.

4. Long-Term Operational Commitment

- Performance monitoring dashboards must track detection accuracy, false positives, and system latency consistently.

- Drift detection mechanisms should trigger retraining cycles when behavioral patterns evolve.

- Support structures must define response times for system anomalies or integration issues.

- Scalability planning should address expansion across regions, products, and transaction volumes.

- ROI evaluation should compare measurable outcomes against original investment objectives.

Long-term operational commitment ensures that Computer Vision in Finance evolves with institutional growth instead of stagnating after initial deployment.

Choosing the right development partner requires disciplined evaluation across workflow alignment, integration engineering, governance maturity, and operational sustainability, especially for organizations planning to hire computer vision developers for regulated financial environments. Institutions that apply this structured assessment framework increase the probability of stable deployment, measurable return, and long-term strategic advantage.

Conclusion

Financial institutions already possess the visual data required to strengthen fraud detection, accelerate onboarding, and improve operational visibility. The real differentiator lies in structured execution.

Computer Vision in Finance delivers measurable results only when architecture, integration, compliance discipline, and business objectives align from the beginning.

Organizations that treat implementation as infrastructure rather than experimentation avoid stalled pilots and fragmented systems.

Investment in artificial intelligence across the financial sector continues to rise because leadership teams recognize the need for intelligent control systems. The real opportunity lies in disciplined execution and the right technical partnership.

Kody Technolab Limited builds custom AI automation platforms designed specifically for financial environments, operating as a specialized computer vision software development company focused on regulated industries. Our deep tech development approach aligns architecture, compliance, integration, and long-term scalability from the beginning.

If your organization plans to implement Computer Vision in Finance, connect with our team to evaluate your roadmap with clarity and confidence.

FAQ

1. How accurate is Computer Vision in Finance for identity verification?

Accuracy depends on data quality, model training discipline, and validation thresholds. Enterprise-grade systems trained on financial document formats can achieve high precision when paired with liveness detection, sanction screening, and structured human review for flagged cases.

2. Can Computer Vision in Finance integrate with existing core banking systems?

Yes, but integration complexity varies. Successful deployments connect extracted document data, fraud alerts, and verification logs directly with onboarding, underwriting, and transaction monitoring systems through secure API frameworks.

3. How long does implementation of Computer Vision in Finance typically take?

Implementation of Computer Vision in Finance depends on scope and integration complexity. A controlled pilot deployment usually requires three to four months, while full enterprise integration across multiple systems can extend to six to nine months.

4. What are the biggest risks in deploying Computer Vision in Finance?

The biggest risks in deploying Computer Vision in Finance include weak data quality, insufficient integration with core systems, unclear business KPIs, and incomplete governance planning. Structured roadmap execution significantly reduces these deployment risks.

5. Is Computer Vision in Finance compliant with regulatory requirements?

Computer Vision in Finance remains compliant when architecture includes encrypted data handling, detailed audit logging, bias testing, sanction screening integration, and regional regulatory alignment based on operational jurisdiction.

6. What tools and technologies power Computer Vision in Finance systems?

Computer Vision in Finance relies on a combination of image processing engines, OCR frameworks, deep learning models, and secure integration layers. Core components typically include document extraction models, facial recognition systems, liveness detection algorithms, anomaly detection engines, API-based integration frameworks, encrypted cloud or hybrid infrastructure, and monitoring systems that track accuracy, drift, and compliance performance.

7. How is ROI measured for Computer Vision in Finance projects?

Return on investment for Computer Vision in Finance projects typically measures fraud loss reduction, decreased manual review cost, faster approval turnaround, and improved operational throughput compared against defined baseline metrics.