The time-consuming, inaccurate, and limited traditional credit check processes create challenges and frustrations for both financial institutions and borrowers. Not only it limits access to credit, but also potentially excludes certain groups of borrowers, implying it’s high time for alternative approaches to credit scoring and lending.

Now, imagine a platform that allows finance providers to evaluate the creditworthiness of a particular person, businessman, or retailer within minutes, without ever setting foot in their home or business premise or going through tedious paperwork.

Well, it’s not a wishful dream – it’s the reality of Credit scoring app solutions.

Credit Scoring App Development,

is where futuristic technologies and modern-day lending practices meet to revolutionize how businesses, manufacturers, retailers, or anyone in need of money access the right amount of credit.

With the rise of alternative credit scoring methods and the increasing popularity of digital lending, credit scoring apps are becoming the go-to solution for financial institutions and businesses looking to streamline their lending processes.

But with the controversy around data privacy and potential bias in algorithms, is this technology all it’s cracked up to be?

In this blog, we’ll dive deep into the world of Credit scoring app development, exploring the latest technologies, the benefits and drawbacks, and everything in between. So buckle up and get ready for a wild ride through the world of digital lending!

What is Credit Scoring? And its Use Cases

Basically, Credit scoring is a statistical method used by lenders to assess a borrower’s creditworthiness, which is the likelihood of the borrower repaying their debts on time. It is based on the borrower’s credit history and other factors that may impact their ability to repay a loan.

Credit scoring is used in a variety of financial contexts, including:

- Loan applications: Lenders use credit scores to determine whether to approve or deny a loan application and to set interest rates and other loan terms.

- Credit cards: Credit card issuers use credit scores to determine whether to approve an applicant for a credit card and to set credit limits and interest rates.

- Insurance: Insurance companies use credit scores to assess the risk of insuring an individual and to set insurance premiums.

However, for finance businesses and FinTechs to provide a credit-scoring app solution, it’s important to understand the following:

- The factors that go into calculating a credit score, such as payment history, credit utilization, length of credit history, and types of credit used.

- The different credit scoring models used by lenders and how they differ from one another.

- The regulations governing credit scoring and how they impact the development of credit scoring apps.

- The importance of data privacy and security in credit scoring app development, as sensitive personal and financial information is involved.

Why develop a Credit Scoring app?

If you look at the digital lending market, it is booming.

The digital lending market size was valued at $10.7 billion in 2021 and is estimated to reach $20.5 billion by 2026, growing at a CAGR of 13.8% from 2022 to 2026.

When the market is growing at such a high rate, so is the demand for fundamental processes. Whether or not to offer mortgages, loans, or other credit products to individuals or small businesses hinges on their credit scores. Besides, a credit score is also a deciding factor for the interest rate and credit limit.

Since the lending process is now digital and faster, a finance company cannot afford to delay the process of validating creditworthiness. It can cost potential customers.

Alternatively, if the company integrates a tech-driven credit scoring app in its lending process, it can proceed with the transaction much faster. For example, if you have developed a Buy Now Pay Later application or Invoice Financing application, you can add a module of credit scoring to accelerate the lending process, enhancing customer satisfaction.

Why is the demand for credit-scoring app development rising?

The COVID-19 pandemic has been a driving force behind the digital lending trend, as many people have been unable or unwilling to visit physical banks or other lending institutions. Instead, they have turned to digital platforms to apply for loans, which offer convenience, speed, and flexibility.

To complement the multi-billion dollars digital lending market’s rapid growth, it is equally important to innovate credit scoring. That’s not it. There are many reasons why digital lenders and Fintech businesses need to integrate credit scoring software. For example;

Edge over Traditional Credit Scoring

Developing a credit scoring app can help address some of the pain points associated with traditional credit scoring methods. For example, traditional credit scoring models often rely on a limited set of data points, such as payment history, credit utilization, and length of credit history. This can result in inaccurate assessments, particularly for those who lack a credit history or have a thin credit file.

By contrast, a credit scoring app can leverage more data points, including non-traditional data such as social media activity or transactional data, to provide a more comprehensive and accurate picture of a borrower’s creditworthiness.

Risk Management

Credit scoring app development can also help lenders improve their risk management capabilities. Lenders can identify high-risk borrowers and mitigate their risk exposure by leveraging more data points and using sophisticated algorithms and machine learning models. This can help them reduce their default rates and increase their profitability.

Customer experience = customer loyalty

A credit scoring app lets a finance provider provide a more seamless and convenient borrowing experience for their customers. By automating the credit scoring process, borrowers can receive loan approvals faster and with less friction, which can lead to higher customer satisfaction rates.

Overall, by leveraging more data points and using sophisticated algorithms and machine learning models, lenders can improve their risk management capabilities and stay ahead of the competition.

What is the difference between Traditional Credit Scoring vs. Alternative Scoring?

You know what credit scoring is, and it’s very important to analyze the creditworthiness of borrowers and decide on loans and interest rates. Now, the next thing you need to understand is the difference between Traditional credit scoring and Alternative Credit Scoring. The difference will intuitively make you understand why credit scoring app software has become a priority for Fintechs.

Traditional Credit Scoring

is based mainly on factors such as an individual’s credit history, current debts, and repayment history. The agency then selects statistical data found in a person’s financial history, analyzes them, and assigns the credit score after the evaluation.

The credit score can be as low as 300 and as high as 850. Evidently, the higher the score, the better. Traditional credit scoring agencies may follow models, and the most famous ones are FICO Model and VantageScore Model.

FICO Model – The traditional credit scoring model has been around since 1989 and is known as the “classic” model that defines the score based on these five factors: Payment History, Credit Utilization, Credit History, Types of Credit, and New Credit.

VantageScore Model – The model was brought in 2006 by credit reporting bureaus to give FICO competition. The model aims to analyze familiar data, such as timely payment, low credit card balance, bank accounts, assets, etc., to evaluate the credit score.

As you see, these systems have been around for a long time and are used by many financial institutions to determine whether or not to give someone a loan or credit.

However, the question arises what if a person is applying for credit for the first time? How will this traditional credit scoring method gauge their creditworthiness when they don’t have any? This rings a bell with the chicken-and-egg story, doesn’t it? Hence, the alternative credit scoring software.

As algorithm-based credit scoring software is an alternate method to evaluate creditworthiness, it is considered an alternative credit scoring method.

Alternative credit scoring,

on the other hand, takes into account even non-traditional factors, such as a person’s job history, education level, and social media activity. The method is designed using AI and ML for the modern world to give lenders a fuller picture of someone’s financial situation and creditworthiness.

So, even if people are applying for the first time, their education, earning, and other financial behavior will be there to speak their creditworthiness.

Consequently, people with little or no credit history, such as young adults, recent immigrants, or small businesses, can access the credit. Moreover, it can help those with a less-than-ideal credit history to prove their creditworthiness based on other factors.

But as you know, no technology escapes without controversies. And alternative credit scoring software is also facing some. Some people worry that it could be used to discriminate against certain groups or that the algorithms used to determine creditworthiness may not be transparent or accurate.

However, many credit-scoring apps have defied such controversies with their bold functionalities, which we’ll discuss further in the blog. Now, let us understand how Fintechs use such alternative Credit scoring solutions.

How do Finance companies use Alternative Credit Scoring solutions?

As discussed, the ratio of digital lending has gone through the roof post-covid, and one of the biggest reasons is a negative impact on everyone’s income. The phenomenon has laid a major drawback on finances and people’s credit scores. Not being able to repay the existing debts makes their credit score even worse.

In such a situation, conducting the traditional credit scoring method is good for nothing. Hence, financial institutes are left with alternate credit scoring that considers more than just previous transactions to define one’s creditworthiness. So how do they apply alternate credit scoring? Let’s find out.

- Finance companies use alternative credit scoring solutions to assess the creditworthiness of borrowers who have a limited credit history or no credit history at all.

- Since alternative credit scoring uses non-traditional data points, such as payment history of utility bills, rent payments, and other financial transactions to generate a credit score for the borrower, finance companies can extend loans to borrowers who may have been denied traditional credit due to a lack of credit history or insufficient credit score.

- Using alternative credit scoring, Fintechs are expanding their customer bases, reducing the credit risk associated with lending money to new and untested borrowers.

- Fintechs can also offer customized financial products and services to their customers based on their credit profile and payment behavior.

- Using alternative credit scoring, Finance companies also gain insights into customers’ spending habits and customize financial plans to help them save more money and manage their finance better.

Basically, by using alternative credit scoring apps, finance companies accelerate the loan approval process, reduce costs associated with manual underwriting, and improve customer satisfaction by providing a faster and more seamless borrowing experience.

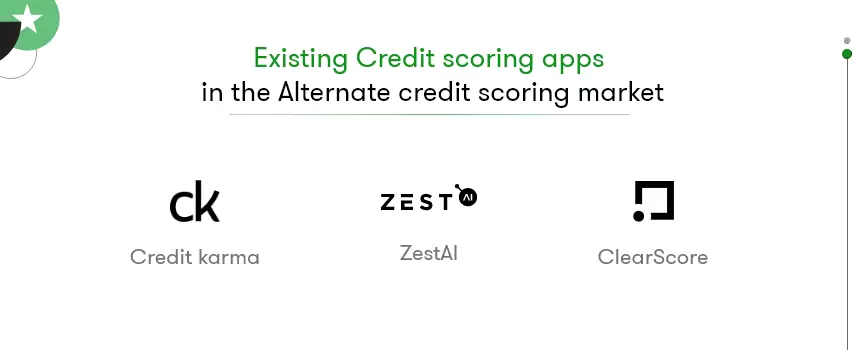

Existing Credit scoring apps in the Alternate credit scoring market

Credit Karma — 2007, San Francisco, US, Total Funding – $868M

Credit Karma is available on both Android and iOS as well as on the web and allows anyone to get access to their credit scores and reports. Basically, the platform utilizes TransUnion and Equifax credit scoring models and provides users with weekly updates on their credit scores.

The platform also recommends a range of financial products to users after analyzing the credit profiles that may help them save money. And if a user buys a financial product, Credit Karma earns from the bank or financial institution, whoever the product the user buys.

Zest AI — 2009, California, US, Total Funding – $300M

A Financial Technology company, Zest AI offers tech-driven solutions for credit underwriting. The company aims to make credit available for everyone and has reputed partners, including Citibank, Suncoast Credit Union, Golden 1 Credit Union, Hawaii USA Federal Credit Union, and more.

Machine Learning-based Zest AI enables lenders to analyze a sea of data and reach out to potential customers to widen their customer base. The company has helped lenders raise approval rates by 25%, reducing charge-offs by 30% to 40%.

Improve business lending decisions with predictive analytics credit scoring powered by real-time data and AI-driven risk insights.

ClearScore — 2014, London, UK, Total Funding – $200M

Used by 18 million across the web, Android, and iOS platforms, ClearScore provides an accurate and reliable credit score and report to improve financial well-being. Furthermore, the company also partners with trustworthy lenders and offers a marketplace of great deals on credit cards, car finance, loans, etc.

There are diverse types of credit scoring apps you can find in the market, and all represent a potential Fintech app idea. If you study more than one type of app, you can plan your credit-scoring software development better. Or, say, make it unique of all.

But where to start developing a credit scoring app?

Developing a credit scoring app requires thorough research and understanding to be able to choose the right technology stack, where to acquire the data, what model to use to score, and whatnot. Let us shed some light on several crucial aspects with details to help you grasp them.

Start with Data acquisition:

First and foremost, a massive amount of data is required for the software to be able to gauge the credit score of its users. Meaning you will need access to reliable and relevant data that can help your model evaluate the credit score accurately. For example, loan repayments, credit card balance, payment history, etc.

You will need to rely on third parties to acquire reliable data to validate others’ creditworthiness (it’s a bit paradoxical, no?). For example, banks, online lenders, credit card companies, credit bureaus, and financial institutions have accurate data. However, it is essential to ensure that the data you acquire is clean, accurate, and up-to-date.

Decide on Features required in a Credit scoring app:

After figuring out where to source the data from, you need to start working on your credit scoring app requirement gathering. This phase includes defining the software’s functional and non-functional requirements as well as its workflow. So, let’s see what some basic features of a credit scoring app are.

Secured login

Allow users to log in with their existing account or sign up with basic details and let them authenticate and secure their account with Touch/Face ID or PIN.

Security Questions

To prevent fraud or unauthorized users from registering on the app, ask the user details to match with data or security questions that only they know.

Analyze Credit Score

Create a dedicated feature that lets users know their credit score with one click.

Track finances

Since you have reliable data sources to fetch and display the data, allow users to track their finances as well as what is affecting their credit scores.

Weekly/Monthly reports

Credit reports are to validate creditworthiness. So, you must have this feature that lets users generate a weekly or monthly credit report.

Alerts

Notifications and alerts are the best way to enhance user interaction on your credit scoring app, and you can improve the app engagement as well by alarming users about any changes in their credit scores.

Credit likelihood

Credit scores are used to take credit, right? But you can make your app more functional with a feature that enables users to analyze the possibilities of their loans or credit requests getting approved.

Credit summary

Leveraging the data you source, create a feature that offers an insightful summary of users’ credit history, including their payment history, credit accounts they have had, credit limits, etc.

Tips and Suggestions

Finance tips and suggestions to improve credit scores can attract more users.

Move ahead with Credit Scoring Model Selection:

Features are important for any app to be functional. But in the case of credit scoring software, credit score evaluating model selection is equally crucial. The model will help you exploit the data to its fullest and provide users with accurate credit scores.

However, different models have different levels of accuracy and complexity as they use distinct data points to calculate the score. Besides FICO and VantageScore, there are some popular models, such as

CreditXpert – widely used in mortgage lending, the tool provides excellent support to lenders to identify potential customers and secure the best rates and terms.

TransUnion CreditVision – the model uses trended credit data and also how borrowers’ credit behavior has been to evaluate creditworthiness.

Experian PLUS Score – unlike traditional FICO credit score, PLUS, which is now part of Experian (a multinational data analytics and consumer credit reporting company), calculates the credit score based on customers’ debt usage, payment history, inquiries for new loans, etc.

So, you will come across many credit scoring models in your research. But it is important to consider the available data and the desired level of accuracy when selecting a model.

Innovate with Cutting-edge Tech Stack:

The tech stack chosen will depend on the specifics of the project but typically includes the programming language, database system, front-end framework, and back-end technologies to be used to develop the credit scoring app. Let us take some technologies, for example.

Mobile App Development

If you intend to develop a credit-scoring mobile app, then you also want to consider the platforms. And if you have decided to cater to both Android and iOS device users, you will have two more options: develop Native apps separately using platform-specific technologies or opt for Cross-platform development that covers both platforms with one single codebase.

Server Side

For the server side means, for the backend of your application, you will need to choose an appropriate programming language, a robust database, and a storage solution. For example,

Programming Languages:

Python – widely used in data analysis and machine learning apps;

R – best for statistical computing, data analysis, and machine learning apps;

Java – reliable and secure for developing enterprise-grade apps.

Database:

You need a database that maintains and process multiple data points efficiently. Some of the most famous are;

- MySQL

- MongoDB

- Firebase by Google

- PostgreSQL

- DynamoDB by Amazon

Find a Good Development Team

“If you deprive yourself of outsourcing and your competitors do not, you’re putting yourself out of business.” — Lee Kuan Yew – Former Prime Minister of Singapore.

The above words said years ago are still applicable given the obsession with being ahead of competitors has increased manifold. Also, outsourcing software projects from offshore development teams are becoming a new norm for a reason.

A great pool of experienced developers, domain expertise, and whatnot at a comparatively low price. Not to mention, hiring a dedicated fintech development team from an offshore company that works solely on your project remotely is way more reasonable than maintaining in-house developers.

However, when hiring dedicated fintech app developers or a technology partner, considering the below factors will help to choose the right ones.

- Stability and reliability

- Development methods they are well-versed with

- Portfolio and current projects

- Industry experience

- Take interviews

- Communication skills

- Analyze client reviews

There is a cheat code to ensure your project doesn’t get into the wrong hands, i.e., consulting before hiring. Almost every software agency offers the first consultation for free, and you can leverage that opportunity to see if the company is worth partnering with.

Kick Start the Credit scoring software development Process

Now that you have your team, you can start developing a credit scoring app that involves developing a user interface, coding the backend, implementing the data sources and credit-scoring model, and keeping everything in sync.

Here are some steps you can take to develop a credit-scoring app:

Design a user interface: Create an intuitive and user-friendly interface for the app, where users can access their credit scores and understand how they are calculated.

You can also turn your app design into a prototype that looks and feels similar to a real-life app. Except, it won’t perform or complete any action on the app as it is just a skeleton and has yet to breathe life in it.

Develop an algorithm: Now, use the data you’ve gathered and develop an algorithm that accurately calculates credit scores.

Backend development: Developers use the programming language and technology stack you selected for backend development that will power your app. During this phase only, the algorithm you develop will be integrated into the backend, and everything will be in sync, including the design, backend, and algorithm.

Test and launch: Now that everything is developed and put together, it’s time to test the app from different angles to ensure accuracy and usability. After performance unit, security, and various app testing, your app will be all set to launch.

Train your model: Your credit scoring app is up and running with its model. Now, you need to train the model so it generates accurate scores fetching the appropriate insights from the data sources.

You can train your model using past credit data, specifically historical customer behavior, credit levels, and payment track records. It is important to validate the model through testing and ongoing refinement to ensure that it delivers accurate credit scores to users.

What are the required Regulations and Compliance to build credit scoring software?

Credit scoring app development requires adhering to certain regulations to ensure legal compliance and protect consumer privacy. Or else your app might be forced to shut down by the government. So, here are some important regulations to consider to save your app:

1. Consumer Credit Protection Act (CCPA): This law regulates the disclosure of credit-related information to consumer credit reporting agencies (CRAs).

2. Fair Credit Reporting Act (FCRA): This act is designed to ensure that consumer credit reports are accurate, complete, and confidential.

3. Gramm-Leach-Bliley Act (GLBA): This act requires financial institutions to protect consumer data and limit the sharing of that data with third-party providers.

4. General Data Protection Regulation (GDPR): This EU legislation regulates the collection, use, and storage of personal data.

Other essential regulations could include state and federal laws regarding consumer protection and data privacy, as well as guidelines from the Consumer Financial Protection Bureau (CFPB) and other regulatory bodies.

So, please consider consulting with legal experts to ensure that your credit scoring app is fully compliant with all relevant regulations.

All things considered, what does it cost to build Credit Scoring Software from Scratch?

Usually, the cost of building a credit-scoring app can vary depending on a number of factors, such as,

- The complexity of the app,

- The number of app features,

- the Technology stack,

- Licensing and regulations,

- Data acquisition,

- Development team’s experience,

- Location of the developers.

However, after researching a variety of credit-scoring software development, we found that a simple credit-scoring app can cost around $10,000 to $20,000. On the other hand, a more complex app with advanced features can cost upwards of $100,000.

Therefore, it is best to consult with a development team or a fintech development company to determine the exact cost of building a credit-scoring app.

Look back; how far have you made it?

You must be so curious to know about credit scoring app development unless you are reading this. We hope the blog will have been a help in understanding the credit scoring app concept. If you enjoyed this, you must check out our much-appreciated post on top Fintech app ideas, where we have compiled a list of billion $ worth of Fintech app ideas.

And if you are into the trending Buy Now Pay Later app development, we have insights on that topic as well as recently booming invoice financing software.

BUT, if you are 100% sure about developing a Credit Scoring app, your next step should consult with our Fintech experts. Delivering tens of Fintech app projects has made our experts genius, and they can help even if you are a blank canvas right now.