Online and mobile channels have become as crucial as branches and ATMs for banks. Increasing demand for omnichannel banking, smart banking, and open banking is driving the banking industry to the edge of digital transformation.

And this digital banking transformation is not limited to a single country but is impacting worldwide banks because banking consumer preferences have changed.

3.3 million people use the internet daily for online banking and 10.8 million several times a week in Germany. Statista.

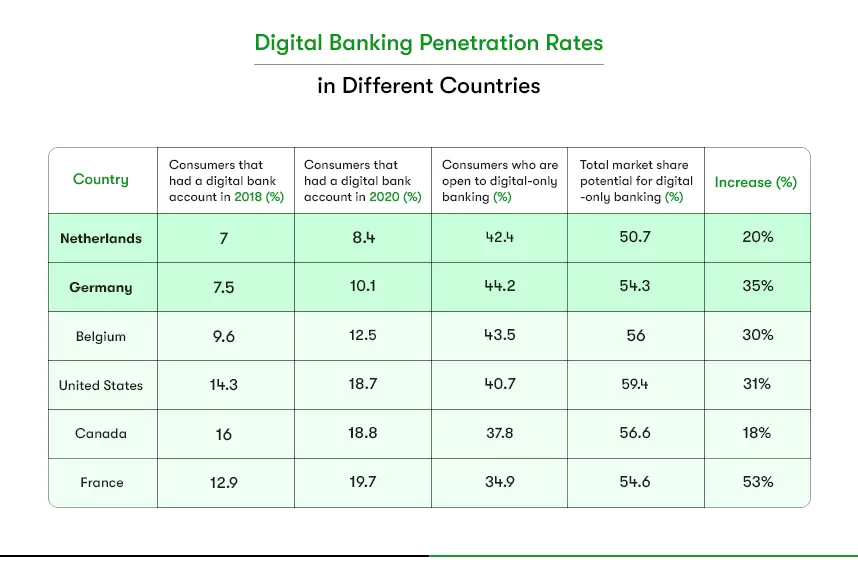

85.7 % of Dutch individuals used online or mobile banking in 2022. Statista.

77% of Canadian customers, 71% of American customers, and 69% of Spanish customers use online banking services at least once a month Global market research.

Evidently, digital transformation in the banking industry is spreading like wildfire. And if being ahead in this competitive industry by providing elite customer experience is your vision as a Bank, you better not be late to embrace digital solutions.

But what exactly does digital transformation for banks mean? And what does a digital banking transformation strategy look like?

Want to know it all? Keep reading on!

What is Digital Transformation in Banking?

Digital transformation in banking refers to leveraging advanced technologies like AI, Data Analytics, Mobile apps, and Cloud computing to revolutionize banking processes. An efficient digital banking transformation strategy can empower banks to provide personalized customer experiences, reduce costs, and improve efficiency, all while gaining a competitive edge.

Cutting-edge technologies used for digital transformation replace traditional manual banking processes with automated and digitized solutions. Consequently, by embracing digital transformation, banks can minimize paperwork and manual intervention. And this automation in routine tasks reduces the hassle for both their employees and customers.

On the other hand, with digital transformation, banks can offer greater convenience and accessibility to their customer. For example, a banking mobile app grants customers complete control over their bank accounts. Since the app is on customers’ smartphones, they can check their balances, transfer money, get banks statement, etc., anywhere, anytime.

This 24/7 accessibility fosters stronger customer relationships and enhances customer satisfaction and loyalty.

In exchange for offering convenience, banks gain something invaluable, i.e., customer data.

Banks collect data through digital channels used by their customers to avail banking services. Applying the right data analytics practices, banks then infer trends in customer behaviors. Ultimately, the data helps banks to identify customer needs and tailor their products and services for different target audiences.

Source: Global Banking Index

What Technologies are used in Digital Banking Transformation and why?

Artificial Intelligence, Machine Learning, Big Data, RPA, and Blockchain are the most used technologies in digital banking solutions. Each technology plays a vital and distinct role in digital transformation. Understanding why you use these technologies will help you choose the right one for your banking transformation.

So, let’s explore technologies used in Digital Banking Transformation and their Roles:

AI & ML (Artificial Intelligence and Machine Learning)

AI and ML refer to technologies that enable machines to mimic human intelligence, learn from data, and make autonomous decisions. Thereby helping banks in enhancing customer experiences and streamline operations.

Use Cases of AI in Digital Banking Transformation:

- Chatbots and Virtual Assistants: AI in banking is used to build chatbots that let banks provide instant customer support and handle routine inquiries.

For example, Bank of America’s Erica, an AI-powered virtual assistant, assists customers with online bill payments to lock and unlock debit cards. Noteworthy, Erica records nearly 1.5 million customer interactions per day.

- Fraud Detection and Risk Management: ML algorithms analyze transaction patterns and customer behaviors to detect fraudulent activities, improving security and reducing financial risks.

For example, using machine learning algorithms, Capital One understands their customer to offer personalized credit limits and identify fraudulent transactions from their customer accounts.

Big Data & Analytics

Big Data and Analytics streamline the collection, storage, and analysis of vast amounts of data from multiple sources. Using big data, banks can derive valuable insights and make data-driven decisions.

Use Cases of Big Data in Digital Banking Transformation:

- Customer Segmentation: Banks use analytics to segment customers based on their behavior, preferences, and needs, allowing targeted marketing campaigns and personalized product offerings.

For example, Citibank uses a Big Data-driven approach to analyze data and target promotional spending, thereby driving business growth and enhancing the services it provides to customers.

- Predictive Analytics: Combining Big data with predictive analytics, banks can predict customer behavior and preferences. Based on the predictions, banks can proactively offer relevant financial products and services.

For example, using predictive analytics, banks can anticipate customer needs and offer tailored financial products based on historical data.

Robotics Process Automation (RPA):

From the umbrella of AI, we have another technology called RPA that possesses the power to mimic human thinking. That makes RPA an ideal solution for banks to automate repetitive tasks, reducing manual efforts and errors and increasing operational efficiency.

Use Cases of RPA in Digital Banking Transformation:

- Account Onboarding: RPA can streamline the account opening process by automating data entry and verification. Using RPA for onboarding, banks can reduce the time required for customers to fully onboard.

- Back-office Operations: RPA bots automate routine tasks in the back-office, such as data reconciliation, compliance checks, and report generation, improving accuracy and operational speed.

For example, German multinational bank, Deutsche Bank and its Blue Water Solution deployed RPA in China for corporate clients to automate repetitive manual tasks, such as transaction processing, reducing processing time and errors. Implementing RPA improves operational efficiency, streamlines workflows, and enhances overall client service.

Blockchain & IoT (Internet of Things):

Blockchain is a distributed and immutable digital ledger that enables secure and transparent transaction recording and verification. Whereas IoT represents a network of interconnected devices that can collect and exchange data over the internet.

Let’s see how Blockchain and IoT can help you in Digital Banking transformation.

Use Cases of Blockchain and IoT in Digital Banking Transformation:

Blockchain for Payments: Blockchain enables faster, more secure, and cost-effective cross-border payments by eliminating intermediaries and enhancing transparency in transaction tracking.

That’s why HSBC harnesses Blockchain power to automatically and securely settle foreign exchange transactions while lowering processing costs and reducing risk.

IoT in Risk Management: Banks can use IoT devices to collect real-time data on insured assets, such as vehicles or properties, enabling more accurate risk assessment and personalized insurance premiums.

For example, Standard Chartered uses IoT devices in their insured vehicles to collect real-time driving behavior and vehicle health data. This data-driven approach enables personalized insurance policies, improved risk management, and reduced fraud, enhancing customer satisfaction and loyalty.

Flutter app development framework

Flutter is a powerful and versatile cross-platform app development framework. You can leverage Flutter to build cross-platform mobile banking apps with a single codebase, reducing development time and costs. This technology also ensures a consistent and smooth user experience across different devices.

Whether you want to create a banking app, wallet app, or customer chatbot app, Flutter offers amazing benefits.

- Cross-Platform Development: Write once, and use it to build the web, Android, and iOS apps.

- Fast and Smooth Performance: Deliver a native-like experience.

- Rich and Customizable User Interface: Tailor apps to meet user needs.

Digital-only bank, Nubank reported, Flutter has been a game-changer, allowing them to continue to scale without sacrificing quality. Many of their engineers have been able to transition to full-stack, increasing developer productivity and enjoyment at the same time.

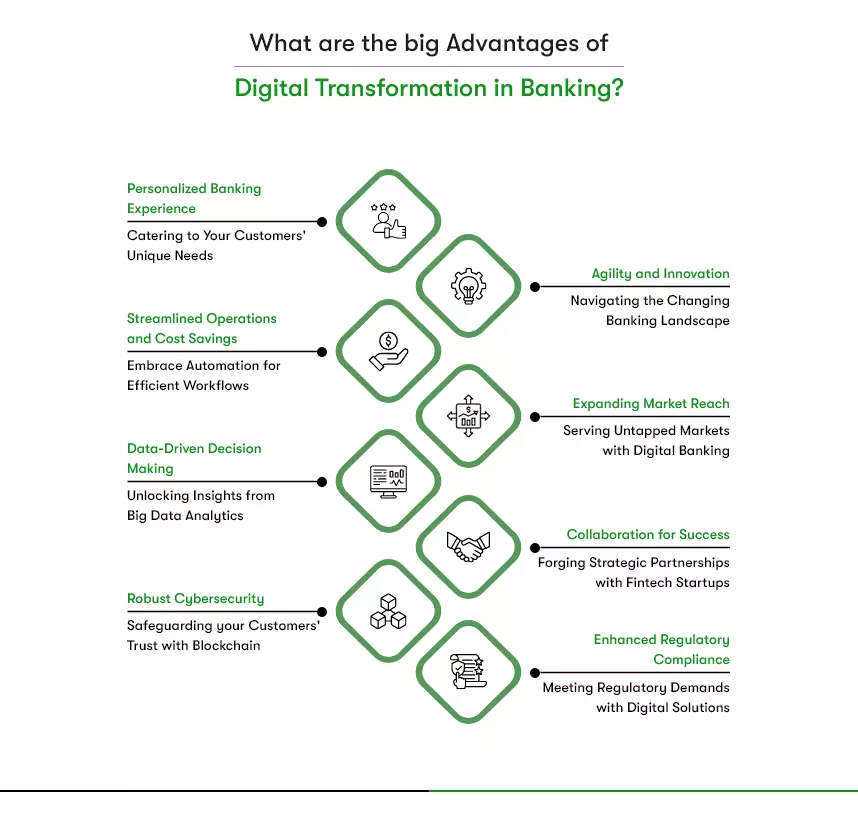

What are the big Advantages of Digital Transformation in Banking?

So, we saw how different technologies play a crucial role in digital transformation strategy, complementing each other. Now, let us shed some light on the benefits of whole Digital Transformation in the Banking Sector.

1. Personalized Banking Experience – Catering to Your Customers’ Unique Needs

Through digital transformation, you can harness AI and machine learning technologies to analyze customer data and preferences in real-time. This allows you to offer tailored product recommendations, targeted offers, and personalized customer support, delivering an exceptional banking experience that resonates with each individual.

2. Streamlined Operations and Cost Savings – Embrace Automation for Efficient Workflows

By incorporating Robotic Process Automation (RPA), you can automate repetitive tasks like data entry and document processing. This frees up your workforce for more strategic activities, leading to increased operational efficiency and significant cost savings.

3. Data-Driven Decision Making – Unlocking Insights from Big Data Analytics

Leveraging big data analytics, you gain valuable insights from customer data, identifying patterns, trends, and preferences. Armed with this knowledge, you can make informed decisions, tailor financial products, and craft targeted marketing campaigns, staying ahead in the competitive landscape.

4. Robust Cybersecurity – Safeguarding Your Customers’ Trust with Blockchain

Digital transformation allows you to fortify security measures with blockchain technology. Its decentralized and immutable nature ensures data integrity and protection against fraudulent activities, earning your customer’s trust in the digital realm.

5. Agility and Innovation – Navigating the Changing Banking Landscape

Embrace Application Programming Interfaces (APIs) to rapidly integrate third-party services and collaborate with fintech partners. This fosters an agile and innovative culture within your bank, allowing you to introduce new features and services, meeting evolving customer expectations.

6. Expanding Market Reach – Serving Untapped Markets with Digital Banking

You can extend your services beyond physical branches through digital transformation, reaching unbanked populations and remote regions. You enhance financial inclusion and expand your customer base by providing digital banking services and mobile apps.

7. Collaboration for Success – Forging Strategic Partnerships with Fintech Startups

Incorporate a collaborative ecosystem by partnering with fintech startups. By integrating their innovative solutions with your infrastructure, you can enhance your service offerings, accelerate product development, and cater to the changing needs of your customers.

8. Enhanced Regulatory Compliance – Meeting Regulatory Demands with Digital Solutions

Digital transformation enables you to implement robust compliance mechanisms, leveraging advanced technologies like AI and big data analytics. By automating compliance checks and monitoring, you can ensure adherence to ever-evolving regulatory requirements, mitigating risks and avoiding costly penalties.

For instance, AI-powered algorithms can monitor transactions in real-time, detecting suspicious activities and potential money laundering patterns. This proactive approach not only safeguards your bank from compliance breaches but also fosters a culture of transparency and trust with regulatory authorities.

Challenges of digital transformation in banking: Common traps to Avoid

Many banks believe that a sufficient technology budget guarantees a successful digital transformation, but that’s not always the case. The banking industry has unique challenges, including technical debt from years of technology investment, complex IT architecture, and a disconnect between business and IT. Additionally, an aging workforce poses obstacles compared to agile fintech.

We have identified these common challenges that hinder banks’ digital transformation and how to overcome them through thorough industry research.

1. Underestimating Complexity and Cost – Plan Strategically:

Banks have historically invested in technology, leading to technical debt and a complex IT landscape. This complexity can make it challenging to execute digital transformation initiatives successfully. Hence, it’s crucial to involve all stakeholders, including business and IT teams, right from the start.

Understand the extent of changes needed and develop a comprehensive strategy to avoid surprises down the road. By setting realistic expectations and planning strategically, you can prevent overrunning your budget and timeline.

2. Miscalculating Technical Debt – Address it Early:

Banks often face the burden of legacy IT applications and infrastructure. However, this technical debt can hinder the creation of a robust digital platform. Ignoring technical debt might seem like a cost-saving approach initially. But it can significantly slow down your digital transformation progress.

That’s why you need to address this technical debt from the outset to ensure that you build a strong foundation for innovation and agility. This way, you’ll be better equipped to effectively meet customer demands and drive digital growth.

3. Struggle in Measuring Impact – Set Clear Metrics:

The banking industry is all about numbers. And it’s no different when it comes to measuring the impact of digital transformation. However, many banks struggle to quantify the success of their digital initiatives.

To overcome this, set clear and specific metrics to measure the impact of each transformation step. Understand how it affects both the top and bottom lines of your bank. By defining success parameters and continuously tracking progress, you’ll be able to demonstrate the actual value of your digital transformation efforts to stakeholders and investors.

4. Slow Pace of Change – Embrace Agile Ways of Working:

The banking landscape has witnessed a surge of agile fintech startups that quickly adapt to market demands. In contrast, traditional banks might find it challenging to match their speed of innovation and product rollouts.

What’s the solution? Embracing agile ways of working to stay relevant in a rapidly changing market of finance. Adopting agile methodologies can help your bank accelerate the implementation of digital initiatives, leading to faster results and a competitive edge.

5. Inefficient Talent – Access Tech Talent:

In the age of digital transformation, tech talent is in high demand, and banks are no exception. While traditional banks excel at hiring banking talent, attracting tech-savvy professionals can be a different story.

However, technology is at the heart of digital banking success. To bridge this gap, redefine your team structure. Outsource a dedicated development team from a reputed and leading banking software development company like Kody Technolab. This is the best way to work with top-notch talent and industry experts who can help you achieve the long-term goals of your digital banking transformation.

6. Silos vs. Synergy – Foster Collaboration:

Banking institutions often operate in traditional silos, with different business units working independently. This fragmented approach can lead to conflicting priorities, a lack of clarity, and inefficiencies.

For successful digital transformation, fostering collaboration across the organization is crucial. Break down these silos and create a unified vision for digital change. Encourage cross-functional teamwork, shared goals, and seamless communication to leverage the full potential of your digital initiatives.

What are Successful Digital Transformation Examples in Banking?

Several banks have successfully undergone digital transformation initiatives to stay competitive in the rapidly evolving banking industry.

ING Bank, Dutch Multinational Bank headquartered in the Netherlands has been a frontrunner in upgrading its digital transformation strategy. By prioritizing mobile banking and embracing innovative technologies like blockchain, ING has consistently innovated its offerings across many countries.

It became the third largest bank in Germany, by introducing ING DiBa, a digital bank for retail banking products and services.

In an interview given to McKinsey, ING’s head of retail market leaders for the Netherlands, Belgium, and Luxembourg, Petri Nikkilä quoted,

If you don’t exist in mobile, you don’t really exist.

JPMorgan Chase embraced a fundamental shift towards customer-centricity by developing a mobile app that offers personalized services and a seamless banking experience. They optimized operational efficiency through automation, leading to improved customer service and resource allocation. The bank fostered a culture of innovation, encouraging employees to embrace technology and find creative solutions.

Based in Singapore, DBS Bank underwent a fundamental shift from a traditional model to a digital-first approach, transforming the entire customer journey into a seamless digital experience. They utilized advanced AI and analytics to gain insights into customer behavior and preferences, driving operational decisions to tailor products and services accordingly. Their mobile banking app, “digibank,” provides a fully digital onboarding process, AI-powered financial insights, and personalized recommendations.

Bank of America also experienced a fundamental shift in customer engagement by introducing an AI-powered virtual assistant named “Erica.” This shift made customer interactions more personalized and convenient. Implementing AI-driven chatbots also improved operational efficiency by handling routine customer inquiries, allowing human resources to focus on more complex tasks.

Buckle up for the Digital Transformation of Your Bank!

Consumers want their banks to be available digitally, empowering them to access their accounts from anywhere, anytime. Because, unlike traditional banking systems where the customers are kept in the waiting room, digital banking solutions prioritize the customer experience. And,

Customer experience is the heart of banking success.

To win this heart, your bank should have a sound digital transformation strategy that also helps you overcome the common pitfalls.

Kody Technolab is a leading software company specializing in digital banking transformation solutions. Focusing relentlessly on innovation and cutting-edge technologies, we empower financial institutions to navigate the digital landscape confidently.

Partner with us to embark on a transformational journey that drives growth and success!