The insurance industry has long been regarded as one of the most traditional sectors, where old conventional processes dominated, and change was not expected. The appearance of Insurtech, a combination of the words “insurance” and “technology”, has forever changed the industry.

Insurtech is the use of innovative technologies to enhance and streamline every aspect of insurance services, from underwriting and claims processing to engaging clients and managing risk. Leveraging Artificial Intelligence (AI), Big Data, Blockchain, and the Internet of Things (IoT), Insurtech is reshaping the way insurance businesses operate and interact with their customers.

In this blog, we’ll explore what Insurtech is, highlight Insurtech examples, and discuss its potential to revolutionize the industry. We’ll also delve into the types of Insurtech, how Insurtech platform’s function, and why they are becoming integral to modern Insurtech business models.

Understanding Insurtech

What is Insurtech?

Insurtech is the application of technological advancements to enhance the efficiency and customer-centricity of the insurance industry. It leverages Artificial Intelligence, Big Data, and Blockchain to predict risks, personalize policies, and streamline claims. Whereas IoT devices, mobile apps, and cloud computing empower insurers to make insurance products accessible anytime, anywhere.

The primary objective of Insurtech is to enable insurers to offer more competitive insurance products and streamline claims processing. It’s all about leveraging modern solutions to give the insurance industry a much-needed makeover.

One crucial technology in Insurtech is AI, which simplifies tasks traditionally performed by human brokers. AI can identify the ideal combination of policies tailored to individuals and streamline the claims management process. Furthermore, Insurtech companies are using these apps, consolidating diverse policies into a single platform, enabling easy management and monitoring.

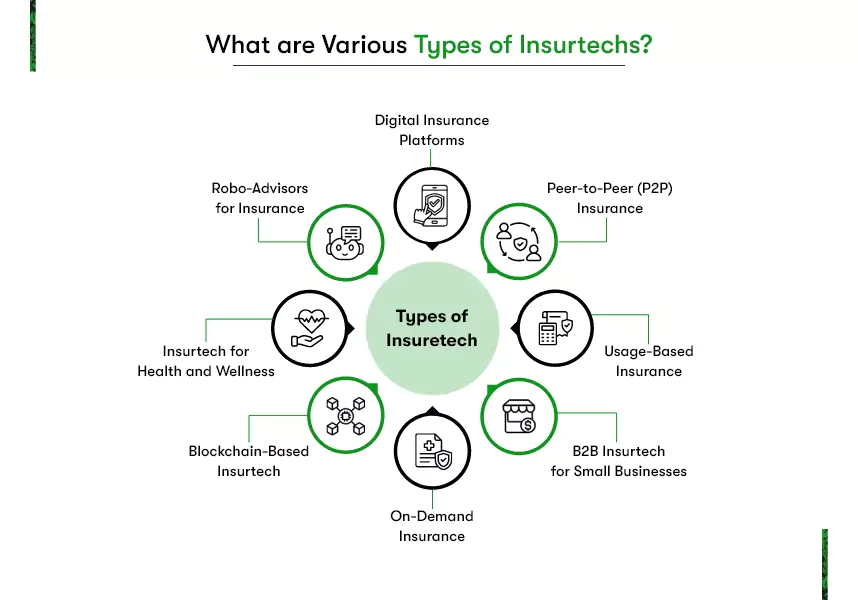

Types of Insurtech

Insurtech encompasses diverse technologies and business models that disrupt and innovate various aspects of the insurance industry. Here are different types of Insurtechs disrupting the industry that require insurance companies’ attention.

Digital Insurance Platforms:

Digital insurance platforms leverage technology to provide insurance products and services online, often focusing on streamlining the customer experience and simplifying the underwriting and claims processes.

For example, Lemonade is a digital insurance platform that uses AI to offer homeowners and renters insurance with automated claims processing, making insurance more accessible and efficient for customers.

Peer-to-Peer (P2P) Insurance:

P2P insurance involves individuals or small groups pooling their premiums to cover each other’s risks. It promotes trust among members and can lead to lower costs and shared benefits.

A good example of P2P insurance is demonstrated by Friendsurance, where friends can form groups to share deductibles. If there are no claims in the group, members receive cashback rewards.

Usage-Based Insurance (UBI):

UBI relies on data from telematics devices or other sources to calculate insurance premiums based on an individual’s behavior or usage patterns. Safe behavior is rewarded with lower premiums.

Progressive’s Snapshot program, for example, tracks driving behavior using telematics and adjusts auto insurance premiums accordingly, encouraging safer driving habits.

B2B Insurtech for Small Businesses:

Insurtech startups catering to small businesses offer digital insurance solutions tailored to the unique needs of entrepreneurs and small business owners.

Next Insurance provides digital insurance products for small businesses, simplifying the purchasing process and offering customized coverage options.

On-Demand Insurance:

On-demand insurance allows customers to activate coverage for specific items or activities when needed, providing flexibility and cost savings.

For example, Trov offers on-demand insurance for individual items, allowing users to insure possessions like cameras or laptops for short periods.

Blockchain-Based Insurtech:

Blockchain-based Insurtech leverages distributed ledger technology to create transparent, secure, automated insurance processes through smart contracts.

Offering decentralized insurance applications based on Blockchain, Etherisc offers parametric insurance products, such as flight delay insurance, with automatic payouts based on predefined conditions.

Insurtech for Health and Wellness:

Health and wellness-focused Insurtech companies use technology to provide additional services and incentives to policyholders to improve their well-being.

Oscar Health, for example, combines health insurance with telemedicine services, digital tools for finding doctors, and personalized health and wellness programs for its members.

Robo-Advisors for Insurance:

Robo-advisors in insurance provide automated recommendations and guidance to customers for selecting products that match their needs and preferences.

Policygenius has already acted on this trend. They use robo-advisors to assist customers in comparing and selecting insurance policies, simplifying the decision-making process.

Any insurance company can transform into an Insurtech leader by incorporating and leveraging the right technologies. Using technologies also allows you to improve customer experiences, create new insurance products, and enhance risk assessment and management processes. Now, let us check out underlying technologies boosting Insurtech across the world.

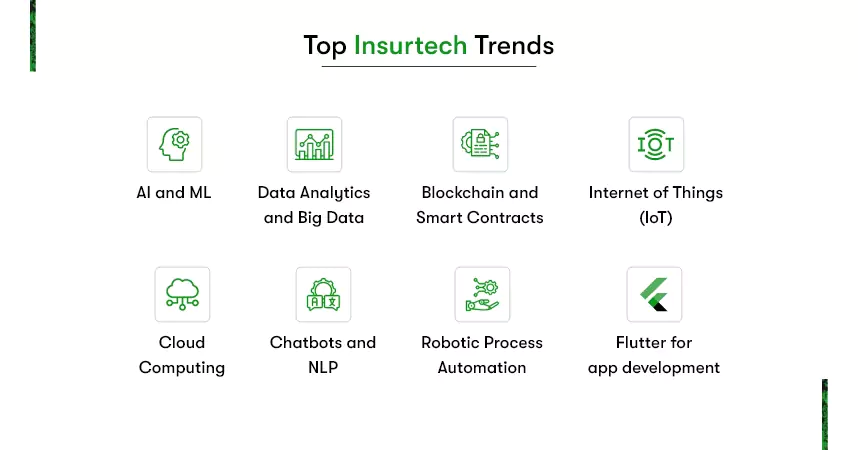

What are Underlying Technologies Driving Insurtech Trends?

Insurtech trends are driven by various technologies like AI, ML, IoT, and more, transforming the insurance industry. These technologies enable insurers and Insurtech startups to innovate, streamline processes, and offer new services.

Artificial Intelligence (AI) and Machine Learning:

Artificial Intelligence (AI) and Machine Learning play pivotal roles in Insurtech. These technologies enable insurers to predict risks more accurately, detect fraudulent claims efficiently, and provide personalized insurance offerings. Additionally, AI-driven analytics analyze vast datasets to enhance risk assessment and customer insights, ultimately improving the insurance experience.

Data Analytics and Big Data:

Data analytics and big data form the cornerstone of Insurtech, enabling insurers to make data-driven decisions. These technologies refine risk modeling, deepen customer understanding, and facilitate personalized policies. With usage-based insurance and tailored offerings, they are driving the transformation of the insurance landscape, enhancing efficiency, and keeping insurers competitive in a data-centric era.

Blockchain and Smart Contracts:

Blockchain and Smart Contracts provide secure and transparent record-keeping for insurance policies and claims. Smart contracts automate processes, reducing the potential for fraud and ensuring swift claims settlements. This technology enhances trust between insurers and policyholders while streamlining policy management and compliance procedures.

Internet of Things:

The Internet of Things (IoT) introduces real-time data into insurance processes. IoT devices, like telematics in vehicles or home sensors, supply insurers with valuable insights for assessing risk and offering customized coverage. This technology results in more accurate risk assessment, personalized pricing, and proactive risk management.

Mobile app:

Mobile Apps and Digital Platforms have made accessing insurance products, managing policies, and submitting claims a breeze for customers. This convenience significantly improves the customer experience by simplifying processes and increasing engagement with insurance services.

Get the inside scoop on How to Develop an Insurance Application

Cloud Computing:

Cloud Computing offers scalability and flexibility to insurers, allowing them to handle massive amounts of data efficiently. This technology reduces infrastructure costs and enables quicker deployment of new services, enhancing data accessibility and processing capabilities.

Chatbots and NLP:

Chatbots and Natural Language Processing (NLP) are vital for customer support. AI-driven chatbots powered by NLP handle customer inquiries, guide users through policy selection, and assist with claims reporting. This results in improved customer service efficiency, round-the-clock support, and quicker response times.

Robotic Process Automation:

RPA automates repetitive tasks within the insurance industry, such as claims processing and underwriting. This technology increases operational efficiency, reduces human error, and leads to cost savings for insurers.

Flutter for app development:

As a robust and flexible framework for app development, Flutter is driving insurance companies towards the next level of customer engagement. Flutter is a cross-platform app development framework facilitating the development of iOS and Android apps from a single codebase.

With Flutter, insurance providers can create sleek and feature-rich mobile applications. These apps empower customers by making insurance products more accessible and user-friendly. The only thing you need to do is hire experienced Flutter developers to develop your insurance app.

The result? A seamless and engaging experience that enhances customer satisfaction and sets a new standard in the digital insurance realm.

AI and Machine Learning contribute to the entire Finance ecosystem. Read here to know more.

What are the challenges of Insurtech that one may encounter?

We can say, for ages, we have been following manual working methods. Be it insurance distribution, underwriting, claim handling, or other operations.

However, InsurTech will dramatically change the entire system and transform the corporate culture and governance.

The regulatory factors will be taken care of, also technologies like RPA will reduce the time consumption for a task. Having said all this, the changes should not hamper the current scenario in a way that people feel uncomfortable during the operation.

You must ensure that the technologies you plan to use should work in favor of your insurance company. Therefore, understanding industry-specific requirements is essential before selecting technology.

Say, for example, if you are using artificial intelligence, it may serve to benefit insurers, but decision-making lies in the hands of humans. Also, you need to ensure that the team of individuals working in the company are tech savvy and have adequate knowledge about implementing technology in the system. Alternatively, you can provide training and help them understand the innovation.

The next significant barrier is privacy. The distributed ledger system spread across various systems puts data at risk. Therefore, you must implement the latest cybersecurity technologies and comply with regulations to ensure data security.

All things considered, why is it so crucial for Insurance Companies to adopt the Insurtech trend? Let’s find out!

What are the Benefits of Insurtech?

The changes technology will bring to the insurance segment will be noteworthy. Ignoring this digital transformation in the insurance industry can cost insurers their customers. According to McKinsey insights, European Insurtechs have the potential to become a €200 billion market by 2030. Here are the various scenarios to describe how it will impact the segment.

- It will boost the customer experience:

Comfort is the main thing that today’s customers seek. By leveraging technology in this segment, customers will have a more personalized experience. They can engage quickly and swiftly over the platform, select their coverage, understand their needs, etc., in an organized manner.

- Insurtech will promote efficiency:

It looks like Insurtech will serve the pain point of the entire Insurance system. Technology assistance will help policy seekers and policyholders to research and explore various policy options over the platform. They can quickly access the information and save hours of man work.

- Insurtech will enhance flexibility:

Insurance companies will now be sorted with the type of experience they wish to provide to the customers. They can now focus on other important tasks instead of running behind covering long-term arrangements.

- It will be a cost-saving option:

In simple words, eradication or lessening of human power will break down the overall cost. Insurance companies will be able to operate remotely without needing to hire staff or place and pay for the same.

- Insurtech will decrease the chances of fraudulent activities:

The main reason why technology is empowering segments is the security factor. Technologies like blockchain and big data will assist insurance companies in keeping track of the activities, saving all the locations, and identifying any inconsistencies.

This way, insurance companies can avoid a big risk of fraud.

How Insurtech is Reshaping Traditional Insurance Business Models

Transition to Customer-Centric Approaches:

Typically, traditional insurance models were quite unbending. The point of the matter is that Insurtech emphasizes personalization and customer-centricity. Customer data can now be used by insurers to propose dynamic pricing, customizable policies, and tailored risk assessments.

Enhanced Collaboration with Insurtech Startups:

Instead of competing, many traditional insurers are going into deals with Insurtech startups to include innovative technologies. These collaborations enable incumbents to enhance their offerings without overhauling legacy systems completely.

Shifts in Workforce Dynamics:

With automation handling routine tasks, the bulk of human resources are being reallocated towards more strategic roles. That way, the freed-up human resources allow insurers to focus on innovation, engaging customers, and growing their businesses.

What are examples of Insurtech?

Digital transformation in the insurance industry is getting hyped up because of emerging Insurtech solutions. Insurtech companies simplify the entire process, from insurance purchases and premium payments to claims, by offering mobile apps. To evaluate further Insurtech’s impact on the industry, let us look into some of the rising Insurance apps in the Netherlands.

AEGON:

AEGON’s Insurtech initiatives have significantly improved customer engagement and operational efficiency, making them a competitive force in the insurance industry. Their use of AI demonstrates the potential for technology to transform traditional insurance processes.

AI for Predictive Analysis: AEGON’s use of AI for predictive analysis is a game-changer. The company can offer highly customized insurance policies by analyzing customer behavior and needs. This not only increases customer satisfaction but also allows for more accurate risk assessment.

AI-Driven Chatbots: Implementing AI-driven chatbots for customer service streamlines the communication process. It enables AEGON to respond to customer inquiries promptly and efficiently, enhancing the overall customer experience.

Zilveren Kruis:

Zilveren Kruis’s Insurtech initiatives have made them more efficient, customer-centric, and effective in managing risk. They demonstrate how AI can enhance both customer service and risk management in the health insurance sector.

AI for Claims Processing: Zilveren Kruis’s use of AI to expedite claims processing is a significant advantage. By automating this critical aspect of their operations, they not only reduce processing times but also minimize the potential for fraudulent claims, ultimately leading to cost savings.

Personalized Insurance Packages: The application of AI to create personalized insurance packages based on individual health risk profiles is a notable achievement. This ensures clients receive coverage tailored to their unique needs, promoting customer satisfaction and retention.

GetSafe:

Getsafe’s journey and achievements exemplify the transformative potential of Insurtech. Their technological innovations have redefined insurance for a digital-savvy audience and achieved high customer satisfaction and trust.

Digital Insurance Pioneer: Getsafe’s journey from being an insurance broker to a digital insurer is remarkable. Obtaining its own insurance license highlights its commitment to the digital insurance space.

Tech-Driven Simplicity: Getsafe’s use of technology to simplify insurance processes is central to its success. Smart bots and automation eliminate complexities, making insurance straightforward and accessible.

If you have a question about how much it costs to develop an Insurance app like GetSafe, access the guide immediately!

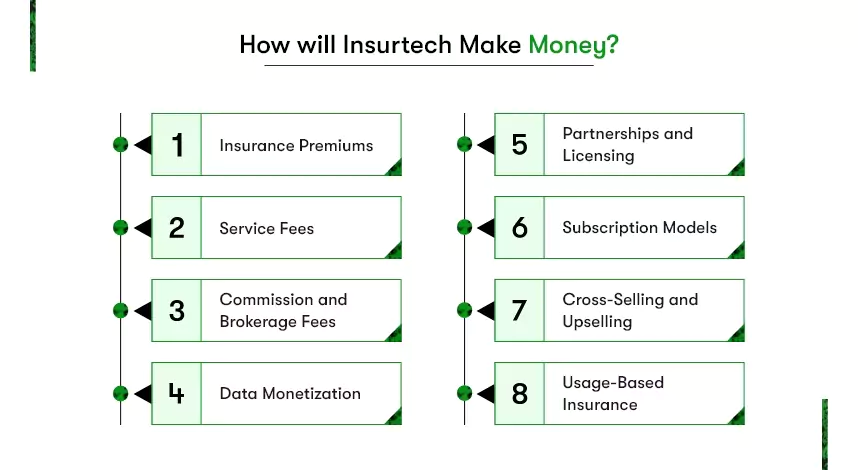

How will Insurtech make money?

Insurtech companies can make money through various revenue streams and business models that leverage technology to disrupt and enhance the traditional insurance industry. Here are some common ways in which Insurtech firms generate revenue:

Insurance Premiums:

This is the most fundamental source of revenue for many Insurtech companies. They sell insurance policies to customers, who pay regular premiums. These premiums provide a steady stream of income, and the pricing of these policies is often based on data-driven risk assessments and customer profiles.

Service Fees:

Insurtech companies may charge service fees for various activities, such as policy administration, claims processing, or providing value-added services. These fees can be a significant source of income, especially when the company offers specialized or tailored services.

Commission and Brokerage Fees:

Some Insurtech companies act as intermediaries or brokers, connecting customers with insurance providers. In such cases, they earn commissions or brokerage fees for facilitating insurance transactions.

Data Monetization:

Insurtech companies often collect and analyze vast amounts of data to assess risks and develop new products. They can monetize this data by selling insights, reports, or aggregated data to other insurance companies, reinsurers, or third-party businesses seeking market insights.

Partnerships and Licensing:

Insurtech firms may enter into partnerships with traditional insurers, leveraging their technology to enhance the capabilities of established insurance companies. These partnerships can result in licensing agreements where the Insurtech firm earns royalties or licensing fees.

Subscription Models:

Some Insurtech companies offer subscription-based services, where customers pay a recurring fee for access to insurance-related tools, risk assessment platforms, or other value-added services.

Cross-Selling and Upselling:

Insurtech companies often use their digital platforms and customer data to cross-sell or upsell additional insurance products or related financial services, earning additional commissions or fees.

Usage-Based Insurance (UBI):

Insurtech companies offering UBI policies charge premiums based on actual usage data, such as driving behavior or IoT sensor data. Customers pay for insurance based on their specific usage patterns.

How does Kody Technolab help Insurance companies?

The insurance sector is growing at a lightning speed. Introducing new technologies seems to make things different, efficient, and effective. With a track record of driving efficiency and effectiveness in the insurance industry, Kody Technolab empowers insurers to stay ahead in this rapidly evolving landscape.

We specialize in tailoring cutting-edge technology solutions to meet the unique needs of insurance companies. Our expertise spans the implementation of AI and ML, Big Data analytics, Blockchain, and IoT, enabling you to streamline operations, enhance risk assessment, and deliver exceptional customer experiences.