Blog Summary: AI budgeting assistants like Cleo are changing how people manage money. This blog explores how to develop an AI budget app that combines automation, personalization, and conversational intelligence. Learn the key features, technology stack, business model, and ROI behind building a next-gen budgeting app that boosts engagement, retention, and financial empowerment.

Picture a digital organism built to understand human spending. It senses income pulses, predicts expenses before they surface, and adjusts saving behavior in real time. This is not a distant concept; it’s what happens when you develop an AI budget app designed to think and act like a financial neural network.

The next generation of budgeting assistants like Cleo represents a shift from passive money tracking to proactive intelligence. They are self-learning systems that adapt to user behavior, merging financial data with context and emotion. The outcome is guidance that feels personal, not programmed.

These innovations are part of the ongoing AI trends shaping the fintech landscape in 2025 and beyond. Conversational AI, predictive analytics, and generative modeling are no longer luxuries; they are the new baseline for digital financial tools. If you plan to build a budgeting assistant that can stand beside Cleo, this guide will walk you through the architecture, features, process, and cost behind it.

What Makes Cleo the Smartest AI Budgeting Assistant?

Cleo is an AI-driven persona that interprets human behavior, personalizes money advice, and responds conversationally. Its intelligence lies in understanding emotion and context, helping users act smarter, not just track smarter.

When you plan to develop AI budget app like Cleo, you’re not copying features; you’re replicating a philosophy. Cleo operates as an adaptive financial coach powered by natural language understanding and real-time analytics. It learns from spending patterns, detects risks, and delivers insights through conversation, not cold numbers.

Unlike static budgeting apps, Cleo uses an intelligent dialogue loop. Every chat becomes a new training signal. It recognizes tone, sentiment, and even procrastination cues to craft nudges that fit a user’s mindset. If someone overspends, Cleo doesn’t scold; it jokes, contextualizes, and helps them recover.

This fusion of AI empathy and financial logic creates trust. Users stay longer because Cleo feels less like software and more like a smart companion. It simplifies the emotional side of money management, a layer many fintech products ignore.

Key aspects that define Cleo’s smartness include:

- Conversational Learning: Continuous intent recognition and context retention make every response relevant.

- Behavioral Analytics: Predicts when users are likely to overspend or miss bills.

- Gamified Savings: Challenges and achievements drive consistent progress.

- Personality Engine: Tone control that balances humor, motivation, and responsibility.

- Financial Inclusivity: Simple language and relatable feedback that engages non-financial audiences.

Cleo proves that modern fintech intelligence is not about data density; it’s about human clarity. If your goal is to make an AI budgeting app like Cleo, focus on human-centered design and adaptive logic. Strong foundations in AI app development enable your product to process emotion, intent, and financial data together. Build for intuition first, algorithms second. That’s what turns data into trust, and trust into lasting engagement.

Why Are Fintech Businesses Racing to Develop an AI Budget App?

Fintech businesses are racing to develop an AI budget app because users now expect financial tools that think, learn, and advise. AI transforms passive money management into an intelligent, real-time experience driving engagement, retention, and higher customer lifetime value.

The Shift from Financial Tools to Financial Intelligence

In the last decade, fintech apps have moved from tracking transactions to interpreting behavior. Earlier, users opened budgeting apps only after making spending mistakes. Now, AI budgeting assistants predict those mistakes before they happen, and that proactive intelligence is what keeps users loyal.

When you explore the scope of AI in fintech, it becomes clear that data is no longer the differentiator; context is. Two users may spend the same amount, but the meaning behind their transactions differs completely. AI models trained on behavioral data, spending intent, and emotional tone can now distinguish between “habit” and “impulse,” turning ordinary notifications into tailored advice.

This behavioral depth allows fintechs to engage users with empathy and timing, a combination that builds trust faster than incentives or interest rates ever could.

AI Creates a Strong Competitive Edge for Fintech Businesses

In fintech, speed and personalization are no longer optional. Every bank, neobank, and finance app operates on similar data streams. The differentiator lies in how intelligently the system processes and responds to that data.

AI budgeting apps outperform traditional systems because they can:

- Predict user needs before requests are made. For instance, suggesting a spending cap before payday instead of showing overspending after it’s too late.

- Simulate financial futures. Users can ask, “What happens if I save $200 more per month?” and get scenario-based projections instantly.

- Automate human-like support. Through natural conversations, AI assistants resolve queries that used to need manual intervention.

- Evolve continuously. Machine learning models learn from every transaction, correction, and conversation, improving precision over time.

This intelligence gives fintech companies not only a user experience advantage but also a data feedback loop that sharpens their business model. Each interaction improves product accuracy, marketing insight, and customer segmentation; all without manual data wrangling.

Business Impact of Developing an AI Budget App

Developing an AI-driven budgeting assistant isn’t just about improving user experience; it’s about transforming economics. Fintech startups that integrate conversational AI see a measurable impact on both operational efficiency and revenue growth.

Operational benefits include:

- Reduced support costs: AI handles 70–80% of tier-one support interactions.

- Improved onboarding: Chat-based walkthroughs simplify KYC and setup, increasing activation rates.

- Automated compliance reminders: The assistant ensures regulatory disclosures are delivered contextually, lowering audit risk.

Revenue advantages include:

- Cross-selling at the right moment: Predictive models recommend credit, savings, or insurance products when they’re genuinely relevant.

- Subscription growth: Premium tiers with advanced insights and savings automation create recurring revenue streams.

- Data-driven innovation: Insights from user behavior drive new product ideas like dynamic saving goals or cash advance models.

This alignment between AI logic and business logic is what makes companies like Cleo, Monzo, and others scale sustainably. They don’t just digitize finance; they personalize it.

How Conversational AI Builds User Trust and Loyalty

What makes users stay with apps like Cleo is not only their accuracy but their personality. The conversational tone transforms the intimidating world of finance into something friendly, inclusive, and even humorous.

When an app uses conversational intelligence to recognize user’s moods, soften difficult messages, and celebrate progress, it builds emotional trust. Users feel seen and supported, not judged. That emotional connection leads to daily interaction, more data sharing, and better decision-making.

Trust, once established, becomes a growth multiplier for every fintech product built with AI at its core.

Essential Features to Include When You Develop an AI Budget App Like Cleo

When you develop an AI budget app, include features that merge automation with empathy like real-time spending insights, predictive savings, and conversational intelligence.

Each feature should simplify financial decisions while strengthening trust through context-aware and emotionally intelligent interactions.

1. Secure and Seamless Account Integration

AI budgeting apps rely on accurate, continuous data flow. Seamless integration with major banks and financial APIs ensures that users can connect accounts safely in seconds.

Essential capabilities include:

- OAuth 2.0 authentication for secure data access.

- Encrypted API connections via providers like Plaid or Yodlee.

- Real-time transaction sync and categorization.

- Multi-bank support for unified financial visibility.

Security remains non-negotiable. Your AI assistant must comply with banking-grade encryption standards and clearly communicate permissions during onboarding. Transparency breeds confidence, and confidence drives adoption.

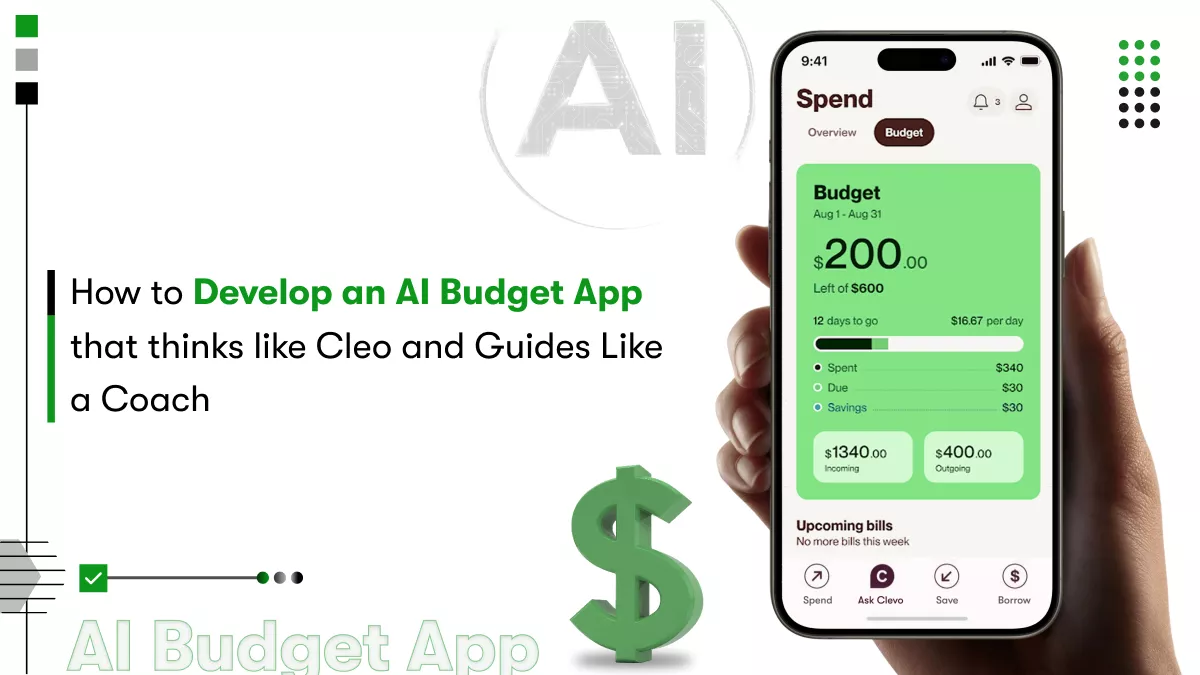

2. Automated Expense Categorization and Smart Insights

Once transactions are fetched, the app’s intelligence begins. Cleo’s appeal lies in its ability to make sense of data instantly, no manual tagging required.

An AI-powered categorization engine should:

- Identify merchants, categorize expenses, and detect anomalies.

- Learn from user corrections to improve accuracy over time.

- Surface weekly and monthly summaries that adapt to user goals.

- Detect recurring patterns like subscriptions or rent.

By blending rule-based logic with machine learning, these systems move beyond data sorting; they generate insights users can act on immediately.

3. Conversational Financial Assistant

The heart of Cleo’s success lies in its chat interface. Users don’t click buttons; they converse. To replicate that experience, design a chatbot that feels natural, empathetic, and intelligent.

Core elements of a smart conversational assistant include:

- Natural Language Understanding (NLU): Accurately interpret user queries, even informal ones.

- Sentiment analysis: Detect frustration or excitement to tailor responses.

- Context memory: Retain conversation history for continuity.

- Adaptive tone: Match personality to user preferences playful, neutral, or professional.

LLMs like GPT-4o or custom fine-tuned models can handle contextual queries such as “How much can I safely spend this weekend?” or “Did I exceed my dining budget last month?”

When conversation feels intuitive, engagement skyrockets and the app becomes part of a user’s daily routine, not just their budget tool.

4. Predictive Analytics and Personalized Recommendations

Modern budgeting apps are not just reactive, they’re predictive. They know when a bill is due or when spending might exceed a limit before it happens.

Incorporate predictive intelligence that can:

- Forecast cash flow based on transaction history.

- Alert users about low balances or irregular activity.

- Recommend saving amounts based on income and habits.

- Suggest achievable financial goals dynamically.

This proactive intelligence turns budgeting from a chore into a guided journey. It helps users stay financially resilient without constant manual input.

5. Automated Savings and Financial Challenges

Cleo gamifies saving, and it works. Users are far more likely to save when it feels interactive and rewarding.

Your AI budget app can replicate that with:

- Smart saving rules e.g., roundups or percentage savings.

- Savings “missions” that challenge users to hit micro-goals.

- Instant progress tracking with celebratory animations or messages.

- Personal benchmarks compared to previous performance.

Gamified saving not only boosts engagement but also builds a positive emotional loop. Every success reinforces consistent behavior, a key metric in financial product retention.

6. Spending Insights and Visualization

People don’t always respond to numbers, but they do respond to stories. Visualizing financial progress transforms abstract data into something tangible.

Include dashboards and summaries that highlight:

- Spending breakdowns by category and timeframe.

- Trend comparisons with past months.

- Personalized “spending scorecards.”

- AI-curated weekly summaries written in conversational tone.

Instead of static graphs, opt for storytelling dashboards, ones that explain why changes occurred, not just what changed. This is how Cleo turns data into daily motivation.

7. Credit-Building and Financial Coaching

Cleo evolved from a budgeting app to a financial wellness coach. Users can improve credit scores, manage cash advances, and receive actionable coaching, all within one ecosystem.

When you plan to develop AI budget app like Cleo, consider:

- Offering secure microcredit or builder card programs.

- Integrating credit score APIs and automated progress tracking.

- Providing AI-based credit advice rooted in spending history.

- Maintaining compliance with KYC, AML, and credit bureau regulations.

These features increase financial inclusivity while strengthening the app’s long-term engagement potential.

8. Privacy, Transparency, and Data Control

The smartest app is useless if users don’t trust it. Privacy-first design ensures users remain in full control of their data.

Key measures include:

- Consent-based permissions for data usage.

- User dashboards to view and revoke access anytime.

- On-device encryption for sensitive information.

- Clear explanations for every AI-driven recommendation.

This approach aligns with global compliance frameworks (GDPR, CCPA, and the EU AI Act), reducing legal risk and enhancing credibility.

9. Push Notifications and Behavioral Nudges

Subtle reminders often create stronger outcomes than strict warnings. AI-driven nudges help users form better habits without feeling overwhelmed.

Examples include:

- Positive reinforcement after completing goals.

- Gentle prompts before predicting overspending.

- Contextual messages like “Your dining budget is 85% used, do you want a summary?”

- Weekly challenges that reward consistency.

Behavioral AI thrives on psychology. The best nudges feel timely, supportive, and human.

10. Scalability and Continuous Learning

An AI budgeting app doesn’t reach perfection on launch, it learns. To sustain accuracy, it must retrain models periodically and scale infrastructure with usage growth.

Ensure your architecture supports:

- Continuous feedback loops from user edits.

- Scheduled retraining pipelines for AI models.

- Cloud-based scalability for real-time data processing.

- Feature monitoring and performance dashboards.

As adoption grows, this continuous learning loop turns your product into a smarter, more intuitive assistant every single day.

Including these ten features ensures your Cleo-style budgeting assistant delivers functionality and emotional resonance in equal measure. Each element contributes to a unified goal that is making finance feel effortless, personal, and empowering.

And before estimating the AI app development cost, it’s essential to understand that quality features and user experience, not just AI sophistication, determine the success and sustainability of your product.

How do AI Budgeting Apps Like Cleo Work?

AI budgeting apps like Cleo operate through a seamless data-to-decision pipeline. They collect financial information, interpret spending behavior with machine learning, and deliver real-time insights through conversational interfaces that feel human, not mechanical.

1. Data Collection and Financial Aggregation

Everything begins with accurate, secure financial data. The app connects to users’ bank accounts using verified APIs. Once linked, it retrieves transaction data, balances, and account histories in real time.

Core process:

- Secure connections: OAuth 2.0 or Open Banking APIs ensure users grant consent safely.

- Real-time sync: Transactions update instantly through aggregation platforms like Plaid or Yodlee.

- Normalization: Data is standardized across different banks and currencies.

By merging accounts and cleaning data, the app forms a single, consistent financial dataset; the foundation for every AI-driven insight that follows.

2. Data Cleaning and Categorization

Raw transaction data is messy. It includes cryptic merchant codes, duplicates, and unclassified items. The next step is data enrichment making financial information understandable to humans.

AI models automatically:

- Identify and label merchants correctly.

- Classify transactions into spending categories.

- Detect recurring payments like rent, subscriptions, or utilities.

- Flag anomalies for potential fraud or unusual activity.

This structured data enables the assistant to move from “numbers” to “meaning,” transforming a stream of transactions into an organized personal finance timeline.

3. Behavioral Understanding through AI

This is where intelligence begins. Each transaction is analyzed not just by category, but by context of when, why, and how users spend.

Behavioral AI engines detect spending rhythms, emotional cues from messages, and recurring decisions.

Over time, they build a behavioral model that answers critical questions like:

- Does the user spend impulsively after payday?

- Are weekends or weekdays more financially risky?

- Which categories trigger emotional spending?

These insights allow the system to personalize advice instead of relying on one-size-fits-all budgeting rules.

Partnering with experts in AI Development Services ensures these intelligence layers are built securely, efficiently, and ethically combining predictive analytics, NLP, and behavioral learning within compliant data architectures.

4. Predictive Analytics and Forecasting

Once the system understands user behavior, predictive AI takes over.

Using past data and contextual patterns, the app forecasts what might happen next.

Examples of predictions:

- Expected balance at the end of the month.

- Probability of missing a bill payment.

- Forecast of next recurring charge or subscription renewal.

- Safe-to-spend limits based on upcoming income and expenses.

This forward-looking intelligence helps users plan rather than react, building a sense of control that typical financial dashboards fail to offer.

5. Conversational Layer and Interaction Logic

The chatbot interface transforms AI insights into natural conversations. Users can type or speak about their queries, and the system translates them into financial actions or summaries.

Core interaction loop:

- The user asks the question, “Can I afford to go out this weekend?”.

- Natural Language Understanding (NLU) interprets intent and entities.

- The AI retrieves relevant financial data.

- A contextual response is generated using LLMs.

- The conversation is logged for learning and future reference.

This conversational layer gives the AI a voice, a brand personality that humanizes data-driven finance.

6. Learning and Feedback Loops

An AI budgeting app never stops learning. Every correction, chat, and click becomes a data point for refinement.

Continuous improvement happens through:

- User Feedback: When a user edits a category or corrects a mistake, the system updates its model weights.

- Model Retraining: AI periodically learns from aggregated anonymized data.

- Behavior Tracking: The assistant measures engagement, trust, and satisfaction to improve its tone and timing.

This self-improving cycle is what makes AI assistants like Cleo feel more intelligent the longer you use them.

7. Personalized Nudging and Action Guidance

Once the app has intelligence and behavioral context, it begins guiding user behavior through personalized nudges.

These nudges are not random reminders; they’re data-driven interventions.

Examples include:

- Your grocery spend is 20% higher than usual this week.

- You could save $150 this month if you cancel unused subscriptions.

- Want me to move $25 to savings today?

Each nudge is delivered with tone and timing designed to feel conversational and helpful, not intrusive. This is where AI meets behavioral psychology, turning awareness into consistent action.

8. Visualization and Storytelling

Numbers alone don’t inspire change; stories do. AI apps like Cleo use narrative visualization to help users see their financial journey.

Instead of static charts, the assistant explains patterns in words:

- You spent 15% less on dining this month- nice work!

- Utilities increased by $30 compared to last quarter.

These summaries are generated dynamically, using AI to craft messages that align with each user’s tone preference and goals.

9. Security, Compliance, and Ethics in Operation

Every process, data retrieval to AI decisioning; must run within the boundaries of fintech compliance frameworks.

To operate responsibly, AI budgeting apps must ensure:

- GDPR and CCPA compliance.

- Clear opt-ins for data collection and usage.

- Transparent AI decision explanations.

- Regular vulnerability assessments and penetration testing.

Ethical design is no longer optional, it’s a requirement for user trust and long-term credibility.

10. Continuous Optimization Through Data Intelligence

The AI ecosystem inside a budgeting app functions as a living network. It monitors KPIs, measures behavioral drift, and identifies where models need refinement.

This continuous optimization covers:

- Predictive model recalibration for new spending behaviors.

- Prompt engineering updates for improved conversational accuracy.

- Regular A/B testing for nudge efficiency and conversion.

The more users interact, the smarter the system becomes, creating a compounding advantage over time.

By understanding this workflow, business leaders can see that developing an AI budgeting assistant isn’t just about writing code; it’s about building an adaptive financial ecosystem. Every part of the system communicates, learns, and improves.

When you develop an AI budget app like Cleo, you’re not just building software; you’re designing a digital organism that evolves with its users, learns from them, and ultimately helps them make better financial choices.

What Is the Business Model for Cleo and How Does It Earn Revenue?

Cleo’s business model combines freemium access with paid financial wellness tools. It generates revenue through tiered subscriptions, affiliate partnerships, and card interchange fees, creating a sustainable system where user trust fuels steady recurring income and measurable growth.

Cleo follows a freemium structure with three paid tiers: Grow, Plus, and Builder. Each offers higher-value features like cash advances and credit-building tools. Subscription revenue drives up most of its earnings, complemented by commissions from partner financial products.

The model succeeds because it aligns user progress with business profit. As users save more and engage longer, revenue scales naturally. For fintech founders aiming to develop an AI budget app, analyzing Cleo’s framework provides a clear path to sustainable monetization and long-term retention.

Tracking the ROI of AI apps helps ensure your investment in intelligent automation translates into consistent financial returns, not just improved user experiences.

Develop an AI Budget App to Shape the Future of Financial Intelligence

AI has changed how people understand money. When you develop an AI budget app, you don’t just automate transactions; you create a digital companion that learns, guides, and empowers users to make smarter financial choices. Cleo’s success proves that intelligence, empathy, and design can coexist to reshape personal finance for millions.

If you’re ready to transform your fintech idea into a high-performing, AI-driven budgeting assistant, Kody Technolab Ltd can help. As a leading Generative AI development company, we build intelligent systems that think, learn, and scale responsibly. Whether you need end-to-end AI architecture or want to Hire AI Developers for specialized integrations, our team ensures your product is secure, compliant, and future-ready.

Let’s create the next breakthrough in financial innovation; one that combines real intelligence with real impact.

FAQs

1. What is an AI budgeting app like Cleo?

It’s a smart financial assistant that uses AI to analyze spending, predict expenses, and guide users through conversational, human-like chats to improve their financial habits.

2. How does an AI budgeting app like Cleo work?

It connects securely to users’ bank accounts, categorizes transactions, forecasts spending, and delivers real-time financial insights through an AI-powered chatbot interface.

3. What features are essential when you develop an AI budget app?

Core features include account integration, automated categorization, conversational AI, predictive analytics, savings challenges, and strong data privacy controls.

4. What technology stack is used to build AI budgeting apps?

Most apps use Python or Node.js, AI frameworks like TensorFlow, PyTorch, and GPT-based NLP models, plus secure APIs like Plaid or Yodlee for account integration.

5. How does an AI budget app like Cleo generate revenue?

Cleo earns through tiered subscription plans, affiliate partnerships, and credit card interchange fees, aligning user engagement with steady recurring revenue.

6. How can Kody Technolab Ltd help develop an AI budget app like Cleo?

Kody Technolab Ltd is a trusted AI app development company which helps fintech businesses design, build, and deploy intelligent budgeting apps with secure architecture and measurable ROI.

Contact Information

Contact Information