“The Buy now pay later bubble is about to burst?” – A question everyone in the fintech sector is asking nowadays.

Once unencumbered by government oversight, the buy now, pay later (BNPL) market is now entering a new phase as regulators worldwide shift their focus to consumer protection and risk mitigation.

As fintech businesses continue to adopt BNPL models, it becomes crucial for them to stay updated with the latest BNPL regulatory changes and requirements.

However, the regulatory landscape of BNPL varies across different countries, with each jurisdiction taking its own approach to addressing the unique challenges associated with these services.

This blog delves into the critical information and impending regulations that fintech businesses operating in the BNPL sector need to know. Let’s equip you with the knowledge to adapt, comply, and thrive in the face of emerging regulations.

Understanding the “Buy Now, Pay Later Bubble About to Burst” Frenzie:

The BNPL bubble refers to the rapid expansion and popularity of BNPL services and the potential risks associated with it. With its appeal to consumers seeking interest-free credit and flexible payment options, BNPL has witnessed significant growth in transaction volumes and venture capital funding.

However, concerns regarding high fees, complex refund processes, and potential negative credit impacts have raised questions about the sustainability and regulation of the industry. This is the reason behind the sentiment – ‘the buy now pay later bubble is about to burst.’ However, it may not be accurate.

Let’s delve into the BNPL Regulations Updates.

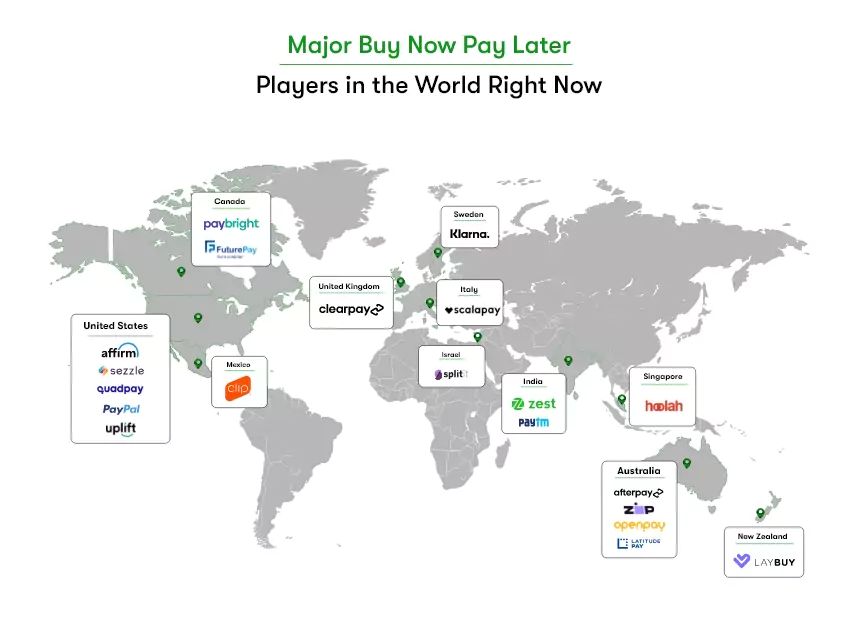

In Australia, regulators aim to make disclosure requirements more consistent across all platforms while allowing flexibility for smaller players. Klarna, one of Europe’s leading BNPL platforms, sees this as positive news because the proposed laws would treat banks, credit card companies, and fintech providers alike.

However, some Australian industry observers think the new rules could favor major incumbents like Afterpay and Zip over more recent entrants like Touch and OpenPay. (1)

An article from Forbes highlights how increased regulation can lead to greater transparency, stricter guidelines, and overall improvement in customer protection. It also mentions initiatives by Visa, Mastercard, and Square to create “white label” versions of their financing products to help merchants offer similar services without working with third parties (thereby reducing reliance on traditional BNPL competitors).

Current Laissez-Faire Environment

The buy now, pay later (BNPL) market has enjoyed a relatively unregulated landscape since its inception, mirroring the trajectory of many other tech sectors. Like ridesharing, streaming media subscriptions, or short-term property rentals, BNPL experienced a surge in popularity. At the same time, governments deliberated on whether to regulate it or not, and if yes, how? This lack of government oversight allowed BNPL providers to operate freely, shaping the market according to their practices and policies.

US Regulation on the Horizon

In the United States, the Consumer Financial Protection Bureau (CFPB) has taken the lead in spearheading BNPL regulation. Recognizing the potential risks associated with BNPL, the CFPB recently released a study shedding light on the dangers consumers may face. These risks include not only the accumulation of debt and overextension, but also the potential unauthorized harvesting of user data by BNPL providers.

Although the specifics of the upcoming regulations remain unknown, industry experts predict that the CFPB will unveil proposed rules in the near future. These regulations are expected to bring BNPL under the same regulatory umbrella as traditional credit companies, subjecting them to similar guidelines and restrictions.

One potential focus may be curbing the amount of data BNPL providers can harvest and leverage from their customers, ensuring enhanced consumer protection.

BNPL Bubble’s Progress in the EU

The European Union (EU) has made significant strides in developing a regulatory framework for BNPL. Following a similar approach to the United States, the EU aims to bring BNPL under existing credit regulations, specifically the Consumer Credit Directive. In 2021, the European Commission approved a revision to the directive, extending its scope to encompass BNPL transactions. These regulatory changes are designed to provide new protections tailored to the mobile-first market.

One notable provision within the revised directive is prohibiting pre-ticked contract agreement boxes, ensuring that consumers actively agree to credit terms. Additionally, the order mandates that all contracts be presented in a mobile-friendly format, enabling users to better understand the terms before deciding to credit. While the European Council announced the finalization of the regulatory language in late 2022, the complete set of regulations is yet to be released.

Impact of BNPL Regulation

The potential impact of BNPL regulation is substantial as governments seek to enforce compliance and protect consumers. In the United Kingdom, pending legislation could grant the Financial Conduct Authority the authority to ban BNPL providers from operating altogether.

BNPL providers must ensure that their affordability checks meet the required standards to avoid severe penalties such as fines, imprisonment, or both. Transparent and accurate communication of loan information to prospective customers will also be crucial.

Outside of the UK, we have already witnessed regulators taking action against BNPL providers that violate rules. Sweden, for example, fined BNPL giant Klarna for breaching GDPR regulations concerning personal data protection.

These instances serve as reminders that compliance with regulations is essential for maintaining business operations and avoiding significant financial and reputational consequences.

Hence, it’s important to note that the impact of BNPL regulations will vary for different providers. Those leveraging customers’ existing credit cards for purchases rather than relying on independent apps already fall under many of the same credit regulations as traditional payment cards.

Consequently, they are less likely to experience significant changes due to the upcoming regulations. However, other BNPL providers must proactively adapt and comply with the anticipated rules to avoid running afoul of the regulatory framework, as Klarna experienced in Sweden.

Actionable Insights to keep your BNPL Business Afloat in the BNPL Regulatory Landscape

While the Buy Now Pay Later regulations may seem intimidating, there are ways you can protect your venture.

Ensuring Consumer Protection and Fair Practices

To protect consumers, BNPL regulations emphasize responsible lending practices. Fintech businesses must conduct thorough affordability assessments to ensure customers can repay their debts without undue financial strain.

Transparency in terms and conditions is vital to avoid any misleading information. Additionally, robust dispute resolution mechanisms must be in place to address customer grievances promptly.

Adapting to Evolving Regulatory Frameworks

The dynamic nature of BNPL regulations requires fintech businesses to adapt quickly and proactively. To stay compliant, companies should implement strategies such as closely monitoring regulatory updates, collaborating with industry peers, and engaging in constructive dialogue with regulators. Building strong partnerships between regulators and industry players can foster an environment of responsible growth and innovation.

Navigating the Changing BNPL Regulatory Landscape

The regulatory landscape surrounding BNPL continues to evolve as regulators aim to strike a balance between fostering innovation and ensuring consumer protection. Therefore, Fintech businesses operating in the BNPL space must stay updated with the latest regulatory requirements and take proactive measures to maintain compliance.

Fintech entrepreneurs and finance businesses operating in the BNPL space should closely monitor regulatory developments in their target markets. Besides complying with existing regulations, adapting to potential regulatory changes based on their BNPL business model is recommended.

By proactively addressing compliance and adapting to the evolving regulatory requirements, you can position your BNPL platform to succeed and maintain trust in an increasingly regulated market.

Contact Information

Contact Information