Payments should be fast, secure, and trustworthy. The moment trust is lost, the system collapses.”

— Jack Dorsey, Co-founder of Square

Did you know that online payment fraud will surpass $343 billion by 2027? This is more than 350% of Apple’s net income in 2021, lost to fraud alone. So, how can businesses secure their transactions? The answer lies in escrow-based payment systems. (Juniperre Search)

To protect revenue and customer trust, businesses need to focus on fraud-proof and secure payment solutions with robust fraud prevention.

That’s why escrow-based secure payment app development is becoming popular. Escrow-based platforms are setting the benchmark for secure payment systems, ensuring transactions are protected until both parties fulfill their obligations. This prevents fraud, ensures compliance, and builds trust. To develop a payment system like Escrow, businesses must integrate:

- Regulatory compliance (PCI DSS, AML, KYC)

- Fraud detection and encryption to prevent cyber threats

- A secure, dispute-free user experience

This guide explains how escrow payment systems work, their security features, cost estimation, and how to hire the right development partner. Whether you are a startup or an enterprise, this will help you develop a secure mobile payment app that scales with your business.

Let’s get started.

What is an Escrow-Based Payment System?

An escrow payment system is a secure transaction where a trusted third party holds funds until both the parties to the transaction have fulfilled their agreed conditions. Instead of sending money, the money is kept in an impartial escrow account so that buyers receive what they paid for and sellers receive payment only after fulfilling the conditions.

Escrow payment systems are widely used in real estate, freelancing platforms, eCommerce, and other high-value transactions where security and trust are of essence. Integrating escrow features in payment systems helps companies prevent fraud, reduce chargebacks, and enhance user trust.

How Does an Escrow-Based Payment System Work?

An escrow-based payment system protects transactions by keeping funds in a middleman account until both sides have fulfilled their contractual obligations. Under the hood, this is accomplished through several stages, including ensuring compliance, avoiding fraud, and resolving disputes automatically.

Step 1: User Registration and KYC Verification

Before using the system, both buyers and sellers must register and verify their identity to comply with financial regulations.

Backend Process:

- Users submit personal information, bank information, and identity documents.

- Identification is authenticated via third-party identity verification services in order to follow KYC and AML regulation.

- Verified profiles of users are then kept within an encrypted database so they may continue with the transactions.

Step 2: Transaction Initiation and Escrow Fund Deposit

The escrow process begins when a buyer initiates a transaction and deposits funds into the escrow account.

Backend Process:

- The buyer enters the transaction details (amount, conditions, deadlines).

- The system generates a unique transaction ID and logs it in a secure database.

- Funds are transferred to the escrow account using an integrated payment gateway.

- A smart contract (if blockchain-based) or rule-based logic ensures the money remains locked until conditions are met.

Step 3: Fund Holding and Seller Notification

Once the funds are secured, the system notifies the seller to fulfill their obligations.

Backend Process:

- The escrow account confirms the deposit and updates the transaction status.

- The seller is notified via email, SMS, or app notifications that funds are secured.

- A time-tracking mechanism starts to ensure the seller delivers within the agreed timeframe.

Step 4: Seller Delivers Product or Service

The seller fulfills their part of the agreement by delivering the product or service.

Backend Process:

- The system records proof-of-delivery (e.g., tracking number, signed document, digital submission).

- If it’s a service-based transaction, the system logs timestamps, work updates, or progress reports.

- The buyer is notified that delivery is complete and must verify the transaction.

Step 5: Buyer Approval and Dispute Handling

Once the buyer receives the product or service, they must approve or dispute the transaction.

Backend Process:

- The buyer confirms receipt through the app’s interface.

- If satisfied, the system automatically triggers the fund release from escrow to the seller.

- If there’s a dispute, the system:

- Freezes the funds to prevent unauthorized withdrawals.

- Escalates the issue to the dispute resolution module for manual review.

- Uses AI in Fintech for fraud detection, analyzing behavioral patterns and transaction history to prevent false claims.

Step 6: Fund Release to Seller

After buyer approval (or dispute resolution), the system releases funds to the seller.

Backend Process:

- The escrow system initiates a payout request to the seller’s linked bank account or wallet.

- The system ensures compliance with financial laws, including AML checks on large transactions.

- A transaction receipt is generated and stored for future reference.

Step 7: Security, Compliance, and Reporting

Throughout the process, the system enforces security measures to prevent fraud and ensure transparency.

Backend Process:

- Real-time fraud detection scans transactions for suspicious activity.

- Compliance reports are generated and stored for auditing.

- All transaction details are logged in an immutable database, ensuring transparency and dispute resolution.

By integrating these backend processes, businesses can develop a secure mobile payment app that guarantees transparency, security, and fraud prevention—just like Escrow or Upwork’s escrow model. With this structured escrow model, businesses can develop a secure payment application that ensures fairness, security, and seamless fund transfers.

The Evolution and Expansion of Escrow in Digital Payments

Escrow has been a cornerstone of secure financial transactions for centuries, originally used in real estate and high-value trade agreements. However, as digital commerce and online transactions grew, so did the need for a more scalable and automated escrow system.

How Escrow Evolved from Traditional Finance to Digital Transactions

Escrow has been around for centuries, originally used in property deals and high-risk financial transactions. However, with the growth of digital payments, the model had to adapt. However, with the rise of digital payments, escrow expanded into B2C markets, making high-value online transactions safer for individual consumers and businesses alike.

Early Days (Pre-Digital Era)

- Escrow services were manually managed by banks, lawyers, and financial institutions.

- Transactions required physical paperwork and often took weeks to process.

Digital Shift (1990s–2000s)

- Online marketplaces like eBay popularized escrow for buyer-seller protection.

- Digital escrow services like Escrow.com emerged, offering automated, faster, and more scalable solutions.

Modern Expansion (2010–Present)

- Gig economy platforms (like Upwork) adopted escrow to secure freelancer payments.

- Cross-border trade and B2B transactions leveraged escrow for international payments.

- Blockchain-based escrow solutions emerged, eliminating intermediaries while ensuring trust.

B2C Expansion (Gig Economy, Marketplaces & P2P Payments)

- Gig economy platforms (Upwork, Freelancer) now use escrow to ensure freelancers get paid securely.

- E-commerce marketplaces use escrow to protect buyers from counterfeit products or scams.

- Peer-to-peer (P2P) transactions in high-value deals, such as selling vehicles, digital assets, or luxury goods, now rely on escrow.

- Cryptocurrency transactions leverage smart contract-based escrow to enable trustless exchanges.

Industries Driving the Expansion of Escrow

With the increasing demand for secure digital transactions, escrow is now a key payment model across multiple industries.

| Industry | B2B Use Cases | B2C Use Cases |

| Freelancing & Gig Economy | Enterprise contracts for agencies and consultants | Individual freelancers and clients on platforms like Upwork |

| E-Commerce & Marketplaces | Large B2B trade deals on platforms like Alibaba | Consumer purchases on eBay, Facebook Marketplace |

| Real Estate & Property | Commercial real estate acquisitions | Home buying, rental security deposits |

| Luxury Goods & Collectibles | Wholesale luxury goods trade | Peer-to-peer sales of watches, jewelry, art |

| Cryptocurrency & Digital Assets | Large-scale institutional crypto trades | Small-scale crypto exchanges, NFT transactions |

How Escrow is Shaping the Future of Digital Payments

The integration of escrow into top finance apps shows its growing relevance in financial technology. With AI-driven fraud detection, faster processing, and enhanced compliance, escrow is becoming a mainstream solution for secure online payments.

Moreover, as businesses invest in money transfer app development, escrow-based payment systems are expected to become more common in peer-to-peer (P2P) transactions, B2B settlements, and cross-border payments.

Escrow is no longer a slow, manual process. It has transformed into a digital-first, automated payment security model, protecting billions of dollars in global transactions. Its evolution continues, with more industries integrating escrow to ensure trust, transparency, and fraud prevention in online payments.

Must-Have Features for Secure Payment App Development Like Escrow

A secure escrow payment app must be built with a well-structured feature set to ensure safe, compliant, and dispute-free transactions. Whether for real estate, freelancing, e-commerce, or high-value transactions, the right features will help establish trust, automate fund management, and prevent fraud.

This section covers the mandatory features every escrow system must have and advanced AI-powered functionalities that improve security, efficiency, and user experience.

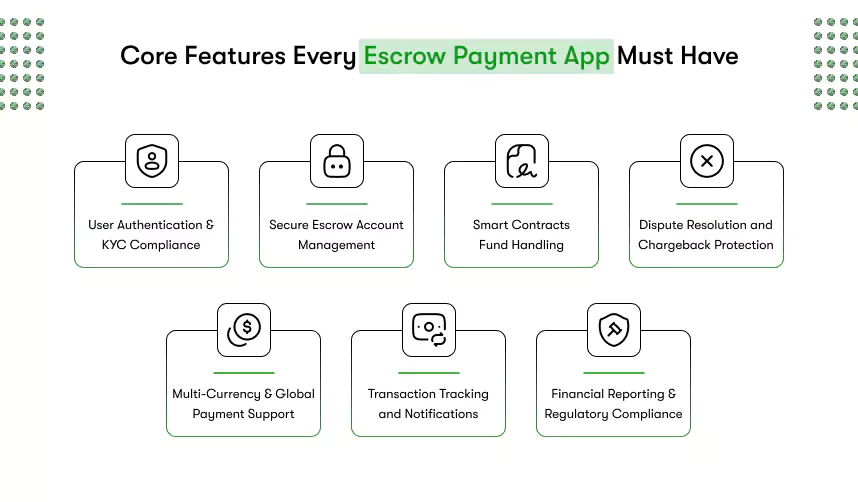

1. Core Features Every Escrow Payment App Must Have

These features form the foundation of any secure payment system development and ensure smooth transactions, compliance, and trust.

User Authentication and KYC Compliance

To prevent fraud and money laundering, the escrow app must have:

- Multi-factor authentication (MFA) to ensure only authorized users can access their accounts.

- KYC (Know Your Customer) verification to validate user identity through government-issued IDs, address proofs, and biometric verification.

- AML (Anti-Money Laundering) compliance to ensure transactions do not involve illegal financial activities.

Secure Escrow Account Management

- Automated fund holding and release to ensure money is securely stored and released only when conditions are met.

- Multi-party transactions that allow buyer-seller-service provider interactions, such as third-party verification.

- Escrow wallet integration to provide users with digital wallets to track funds and transaction history.

Smart Contracts or Rule-Based Fund Handling

- Smart contracts for blockchain-based escrow that ensure transactions are executed automatically when predefined conditions are met.

- Automated rules for fund release using pre-configured conditions to decide when payments are approved or refunded.

Dispute Resolution and Chargeback Protection

- In-app dispute management system that allows buyers and sellers to report issues within the app.

- Escalation to human moderators if AI-based resolutions fail, allowing manual review of disputes.

- Fraud prevention protocols where suspicious disputes trigger additional verifications before fund release.

According to a study by Chargebacks911, businesses lose nearly $125 billion annually due to false chargebacks.

Multi-Currency and Global Payment Support

- Payment gateway integration with Stripe, PayPal, Braintree, or direct bank transfers.

- Multi-currency and cryptocurrency support to allow transactions in various currencies, including crypto, for cross-border payments.

- Real-time currency conversion that automatically converts amounts based on exchange rates.

Transaction Tracking and Notifications

- Live transaction tracking so users can monitor escrow payments in real time.

- Automated push notifications, SMS, and emails for alerts related to deposits, approvals, and fund releases.

- Proof of delivery verification that syncs with logistics services for real-time delivery updates.

Financial Reporting and Regulatory Compliance

- Auto-generated invoices and tax compliance features to ensure financial transparency.

- Detailed transaction history logs that help with audits and dispute resolution.

- GDPR, PCI DSS, and AML compliance to ensure adherence to global financial laws.

PCI DSS compliance reduces payment fraud by 50 percent, according to a report by Verizon.

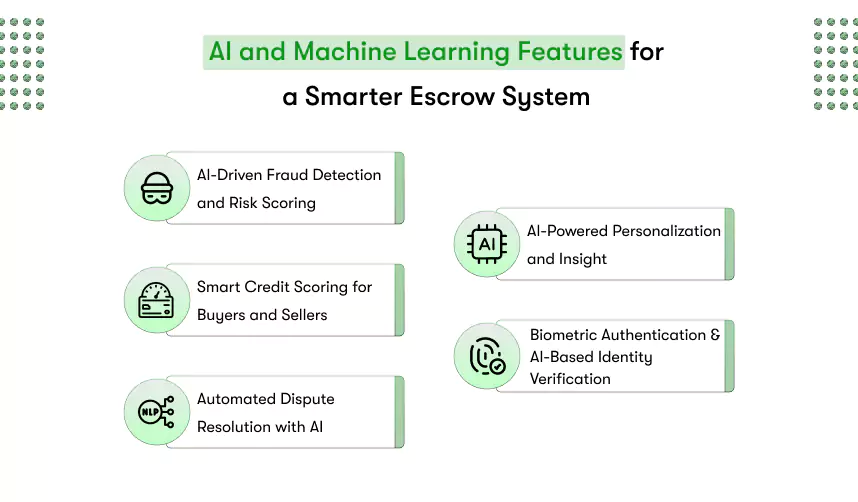

2. AI and Machine Learning Features for a Smarter Escrow System

To enhance security, fraud detection, and automation, escrow payment apps are now integrating AI and machine learning. These advanced features improve efficiency, automate risk management, and personalize user experiences.

AI-Driven Fraud Detection and Risk Scoring

- Machine learning fraud detection that analyzes transaction patterns to detect anomalies.

- Risk-based authentication that flags high-risk transactions for additional verification.

- AI-powered chargeback prevention that detects friendly fraud and protects merchants.

PayPal uses AI-driven fraud detection to analyze over 1,000 data points in real time for each transaction.

Smart Credit Scoring for Buyers and Sellers

- AI-driven credit risk analysis evaluates user trustworthiness based on past transactions.

- Essential for loan lending app development as it assesses repayment capability before lending escrow-backed funds.

- Behavioral analytics that detects patterns of fraudulent sellers or buyers.

Automated Dispute Resolution with AI

- AI-driven case prioritization that assigns urgency levels to disputes based on risk factors.

- Natural language processing (NLP) that analyzes buyer-seller communications to detect fraud.

- Automated resolution recommendations that suggest fair solutions based on historical dispute data.

AI-based dispute resolution systems reduce resolution times by 61 percent, according to Gartner.

AI-Powered Personalization and Insights

- Automated financial analytics that provides users with insights on spending habits and transaction trends.

- Personalized fund management suggestions that use AI to offer recommendations for better financial planning.

- Predictive transaction approvals where AI determines the likelihood of successful transactions based on user history.

Biometric Authentication and AI-Based Identity Verification

- Face recognition and fingerprint authentication for enhanced login security.

- AI-based liveness detection that prevents deep fake identity fraud.

- Continuous user monitoring that detects suspicious behavior even after login.

A study by IBM shows that biometric authentication reduces unauthorized account access by 75 percent compared to passwords.

To develop a secure, future-ready escrow payment app, businesses must combine essential financial security features with advanced AI-driven fraud detection, automation, and compliance management. As AI and machine learning continue to revolutionize financial technology, escrow platforms will become even more efficient, fraud-proof, and user-friendly.

Best Technology Stack for Secure Payment App Development Like Escrow

Building a secure payment app development solution requires a structured, scalable, and secure technology stack. The right backend, frontend, database, security, and payment integrations ensure fraud prevention, seamless transactions, and regulatory compliance.

Businesses must carefully choose the right technologies to develop a secure mobile payment app that can handle high transaction volumes while maintaining security and compliance.

This section explains the technologies required to develop a payment system like Escrow, covering backend frameworks, frontend tools, database choices, payment gateways, and security measures.

1. Backend Development: The Foundation of a Secure Payment System

The backend is responsible for holding funds, verifying transactions, ensuring compliance, and managing disputes. It must be scalable, highly secure, and optimized for real-time processing.

Recommended Backend Technologies

| Technology | Purpose | Why Use It? |

| Node.js | Server-side scripting | Manages concurrent escrow transactions efficiently |

| Django (Python) | Web framework | Offers built-in security and scalability |

| Spring Boot (Java) | Enterprise-grade applications | Best for high-security financial applications |

| Ruby on Rails | Web application framework | Fast development and strong API support |

| Express.js | Lightweight backend framework | Works well with Node.js for building scalable APIs |

For secure payment system development, the backend must also support multi-party fund management, AI-powered fraud detection, and real-time transaction verification to prevent chargebacks and unauthorized transactions.

2. Frontend Development: Ensuring a Secure and User-Friendly Interface

A secure payment application development needs a responsive and intuitive frontend that enables users to manage escrow transactions effortlessly.

Recommended Frontend Technologies

| Technology | Purpose | Why Use It? |

| React.js | Web frontend | Delivers high-performance and interactive user interfaces |

| Angular | Web frontend | Great for enterprise-grade applications |

| Vue.js | Web frontend | Lightweight and flexible |

| Flutter | Mobile app development | Supports cross-platform mobile app development |

| Swift (iOS) | Native iOS development | Optimized for Apple’s security framework |

| Kotlin (Android) | Native Android development | Secure, fast, and recommended by Google |

For businesses planning to develop a secure mobile payment app, the frontend must include secure authentication, encrypted communication channels, and seamless transaction tracking.

3. Database Management: Securely Storing Transactions and User Data

A payment system like Escrow requires a highly secure and encrypted database to store financial transactions, user records, and compliance data.

Recommended Database Technologies

| Technology | Purpose | Why Use It? |

| PostgreSQL | SQL database | High security and compliance for escrow transactions |

| MySQL | SQL database | Reliable and widely used in fintech applications |

| MongoDB | NoSQL database | Handles large transaction volumes efficiently |

| Redis | Caching system | Reduces database load for high-speed processing |

| Amazon DynamoDB | NoSQL database | Serverless, scalable, and highly secure |

4. Payment Gateway Integration: Processing Secure Transactions

A developed payment system like Escrow must integrate with trusted payment gateways that support multi-currency transactions, fraud detection, and chargeback protection.

Recommended Payment Gateways

| Payment Gateway | Why Use It? |

| Stripe | Supports escrow-based payments with high-level security |

| PayPal | Trusted worldwide for secure digital payments |

| Braintree | Best for managing marketplace and escrow transactions |

| Authorize.net | Provides strong fraud protection tools |

| Adyen | Supports global payments with compliance management features |

A report by Stripe confirms that they process over $640 billion in transactions annually, making it one of the most widely used payment processors.

5. Security Technologies: Ensuring Safe and Fraud-Proof Transactions

Security is the most critical factor in secure payment application development. Without strong security layers, fraud risks increase, and transactions become vulnerable to hacking.

Key Security Technologies

| Security Feature | Technology Used |

| Data Encryption | AES-256, SSL/TLS |

| Fraud Detection | AI-driven anomaly detection |

| Two-Factor Authentication (2FA) | Google Authenticator, Twilio |

| Identity Verification (KYC/AML) | Jumio, Onfido, Trulioo |

| Blockchain (Optional) | Smart contracts for automated escrow transactions |

A developed payment system like Escrow must be built with strong backend infrastructure, secure frontend frameworks, reliable databases, and advanced security protocols.

Businesses looking to develop a secure mobile payment app should focus on fraud prevention, regulatory compliance, and seamless user experience.

Cost Breakdown for Developing a Secure Payment App Like Escrow

Developing a secure payment app development solution like Escrow requires advanced security, compliance, fraud prevention, and seamless user experience. The total development cost varies based on technology stack, region, features, and hiring approach.

This section provides a detailed cost breakdown based on development components, regional pricing, and feature complexity.

1. Cost Breakdown by Development Components

Each component of secure payment application development plays a critical role in overall cost estimation. Below is an accurate breakdown based on real industry data.

| Development Component | Estimated Cost (USD) | Time Required |

| Backend Development | $30,000 – $70,000 | 3 – 6 months |

| Frontend Development (Web & Mobile) | $25,000 – $60,000 | 3 – 5 months |

| UI/UX Design | $10,000 – $25,000 | 1 – 2 months |

| Project Management | $8,000 – $20,000 | Throughout |

| Quality Assurance & Testing | $15,000 – $40,000 | 2 – 4 months |

| Security & Compliance (PCI DSS, AML, KYC) | $20,000 – $50,000 | Ongoing |

| Third-Party API Integrations (KYC, Fraud Detection, Payment Gateway) | $12,000 – $30,000 | 1 – 2 months |

| Total Development Cost | $120,000 – $295,000 | 6 – 12 months |

The cost to develop a secure mobile payment app varies based on complexity. A basic MVP costs less, while a full-scale escrow system with AI-based fraud detection and multi-currency support will be more expensive.

2. Cost Breakdown by Region

Development costs vary significantly based on geographical location. Below is an accurate hourly rate comparison and total cost estimate based on real software development pricing from multiple sources.

| Region | Hourly Rate (USD) | Estimated Cost for Full Development |

| United States & Canada | $100 – $150 | $180,000 – $350,000 |

| United Kingdom & Western Europe | $80 – $130 | $150,000 – $300,000 |

| UAE & Middle East | $60 – $120 | $120,000 – $250,000 |

| Eastern Europe (Poland, Ukraine, Romania) | $40 – $80 | $90,000 – $200,000 |

| India & South Asia | $25 – $60 | $70,000 – $150,000 |

Businesses looking to develop a payment system like Escrow at a lower cost often outsource development to Eastern Europe or South Asia, where rates are lower but expertise remains high.

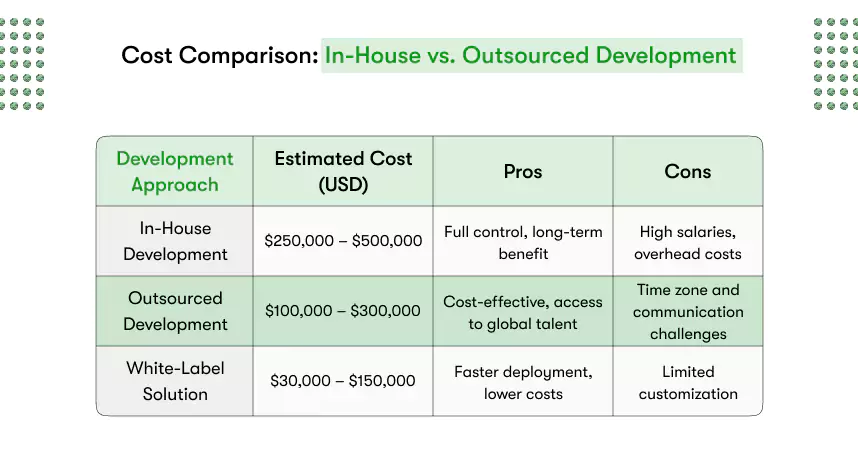

3. Cost Comparison: In-House vs. Outsourced Development

For businesses planning to develop a payment system like Escrow, the total cost depends on the hiring model. Below is a verified cost comparison based on real industry salaries and outsourcing rates.

| Development Approach | Estimated Cost (USD) | Pros | Cons |

| In-House Development | $250,000 – $500,000 | Full control, long-term benefits | High salaries, overhead costs |

| Outsourced Development | $100,000 – $300,000 | Cost-effective, access to global talent | Time zone and communication challenges |

| White-Label Solution | $30,000 – $150,000 | Faster deployment, lower costs | Limited customization |

For companies planning to make a payment system like Escrow, outsourcing is the most cost-effective option, while in-house development is better for long-term product expansion.

The cost to develop a secure mobile payment app varies based on development complexity, region, and features. Businesses should carefully analyze their budget, security needs, and scalability goals before making a decision.

Conclusion: Build a Secure, Trustworthy Payment App Like Escrow

Developing a secure payment app development solution like Escrow goes beyond transactions, it’s about trust, security, and compliance. From AI-driven fraud detection to automated dispute resolution, every feature must work seamlessly to ensure safe and dispute-free payments.

A secure payment system development protects businesses from fraud, chargebacks, and regulatory risks, making it a must-have for industries handling online transactions.

At Kody Technolab, we specialize in developing secure mobile payment apps with cutting-edge escrow solutions, AI-driven security, and regulatory compliance. Our expert team ensures your payment platform is scalable, fraud-resistant, and built for global transactions.

Ready to develop a secure payment application that users trust? Partner with Kody Technolab today to build a future-ready escrow payment system.

Contact Information

Contact Information